Introduction

Most businesses focus on revenue, profit, and growth. Cash reserves rarely get the same attention. That is a mistake.

A cash reserve account (or a business savings account) is one of the most practical tools a business or individual can have. It provides a financial cushion when things do not go to plan, and it gives you the confidence to make decisions without short-term panic.

This guide explains what a cash reserve account is, how much you should hold, and how to build one in a way that works for your situation.

What Is a Cash Reserve Account?

A cash reserve account is a pot of money set aside specifically to cover unexpected costs or periods when income falls short. It is not your day-to-day operating account. It is kept separate and only drawn on when genuinely needed.

For businesses, this might mean covering payroll during a slow month, replacing equipment that fails without warning, or bridging a gap while waiting for a large customer invoice to be paid.

The account itself is typically a business savings account or an instant access deposit account. The goal is not to earn significant interest. The goal is to keep the money accessible and separate from your working capital.

The idea of a cash reserve account is that you don’t need to access the funds in the course of normal trading. Only when something adverse happens should you be looking to access the Cash Reserve account.

Who Needs a Cash Reserve Account?

The short answer is almost everyone. But the amount and purpose will vary depending on your circumstances.

Businesses & SMEs:

Cash flow is the number one reason small businesses fail. Even a profitable business can run into serious trouble if it cannot cover its costs during a difficult few weeks.

A cash reserve gives a business breathing room and a business owner peace of mind. It means a late-paying client or an unexpected cost does not immediately threaten the ability to pay staff or suppliers.

Self-Employed Professionals:

If you are self-employed, your income is variable. There is no employer covering your salary during a quiet month or if you are unwell.

A cash reserve also helps with tax. Self Assessment deadline & bills can feel large when they arrive in January. Setting money aside throughout the year, and holding it in a dedicated account, makes that moment far less stressful.

Is a Cash Reserve the Same as a Cash Buffer?

These terms are often used interchangeably, and for most practical purposes they mean the same thing, being money kept aside to absorb financial shocks.

There is a subtle distinction sometimes made in financial planning. A cash buffer tends to refer to money kept in or near your operating account to smooth day-to-day fluctuations. A cash reserve is a slightly more formal pot, held separately and treated as off-limits except in genuine emergencies.

However, here I’ll use the two terms as interchangeable. What matters is that the money exists, it is accessible, and it is not mixed up with your everyday spending.

Cash Runway vs Cash Buffer: What Is the Difference?

These are related but different concepts, and it is worth understanding both.

- Cash runway is how long your business can survive at its current rate of spending if no new income comes in. It is calculated by dividing your available cash by your monthly outgoings. For example, if you have £60,000 in the bank and your costs are £10,000 per month, your runway is six months.

- A cash buffer is the reserve you hold on top of your operating cash to handle unexpected costs or short-term income gaps. It is not the same as runway. Runway measures survival time. A cash buffer is a specific amount of money set aside for resilience.

Both metrics matter. Knowing your runway tells you how exposed you are. Having a cash buffer reduces that exposure.

The two interact because the shorter your Cash Runway, the more funds you would consider formally keeping and reserving in your Cash Reserve.

How Much Should You Hold in a Cash Reserve Account?

There is no universal answer. The right amount depends on the nature of your business, the predictability of your income, and your fixed cost base.

As a general starting point:

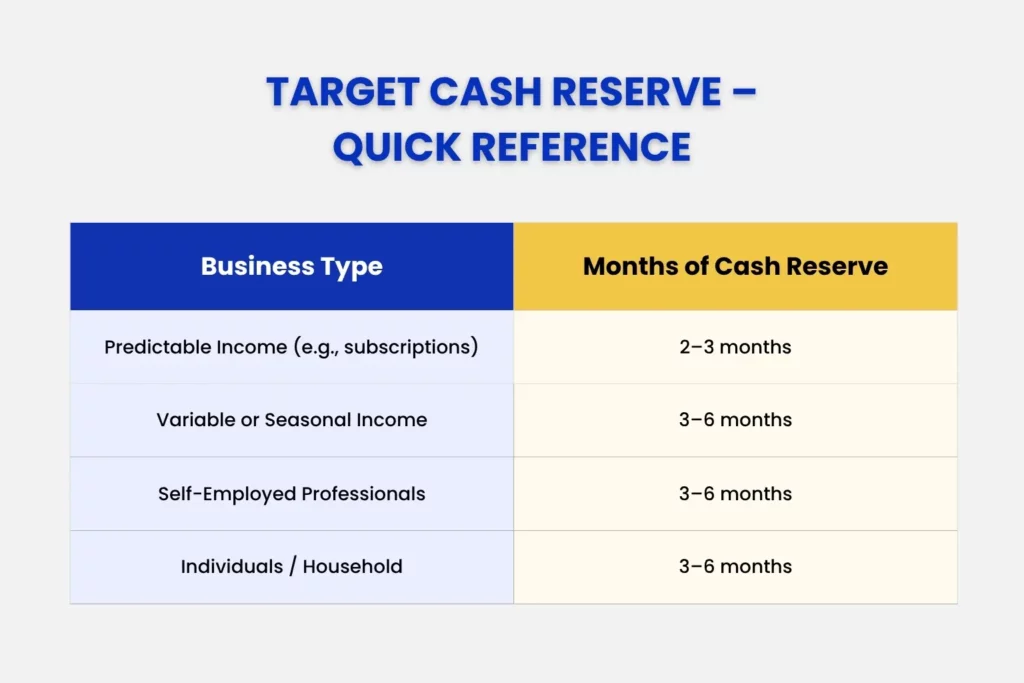

- Businesses with predictable, recurring revenue (such as subscription or retainer-based models) can often operate comfortably with two to three months of fixed costs in reserve.

- Businesses with variable or seasonal income should aim for three to six months of fixed costs.

- Self-employed individuals are typically advised to hold three to six months of personal and business expenses combined.

- Individuals should hold three to six months of essential household outgoings.

To put a number on it: if your business fixed costs are £15,000 per month, a target reserve of £30,000 to £45,000 gives you two to three months of cover. That is a meaningful safety net without tying up excessive cash that could otherwise be working for the business.

The right figure for your business is something worth discussing with your accountant, particularly as the business grows and your cost base changes.

How to Build a Cash Reserve Account

Building a reserve does not happen overnight. The key is to start small and be consistent.

- Set a target. Decide how many months of costs you want to hold. Start with one month as your first milestone if the full target feels out of reach.

- Open a separate account. Keep the reserve completely separate from your day-to-day business account. Out of sight helps keep it out of reach.

- Automate the contributions. Set up a standing order to move a fixed amount into the reserve account each month. Treat it like any other business cost.

- Use windfalls wisely. A strong month, a one-off payment, or a tax refund are all opportunities to accelerate your reserve. Put a portion straight into the account before it gets absorbed elsewhere.

- Review it regularly. As your cost base changes, your target reserve should change too. Review the figure at least once a year. Here, professional cash flow services & budgeting can do wonders.

- Do not dip into it for non-emergencies. Define what qualifies as a genuine emergency before you need to make that call. The more clearly you set the rules upfront, the less tempting it is to raid the pot.

What If You Do Not Have Enough Cash Reserves?

Many businesses operate with little or no cash reserve, particularly in the early years. If that is your situation, the first step is to understand why.

In some cases, the business is simply not generating enough surplus to set anything aside. That points to a profitability or pricing issue that needs addressing at the root.

In other cases, cash is being absorbed by growth, by slow-paying clients, or by costs that have crept up without a corresponding review. A cash flow forecast can help identify where the money is going and where savings or improvements are possible.

If you need to cover a short-term gap while you build reserves, there are options available

Emergency Business Funding Options (When Cash Reserves Run Low)

If your reserves are depleted and you are facing a cash shortfall, the following options are worth considering. None of them are substitutes for having reserves in place, but they can help bridge a gap.

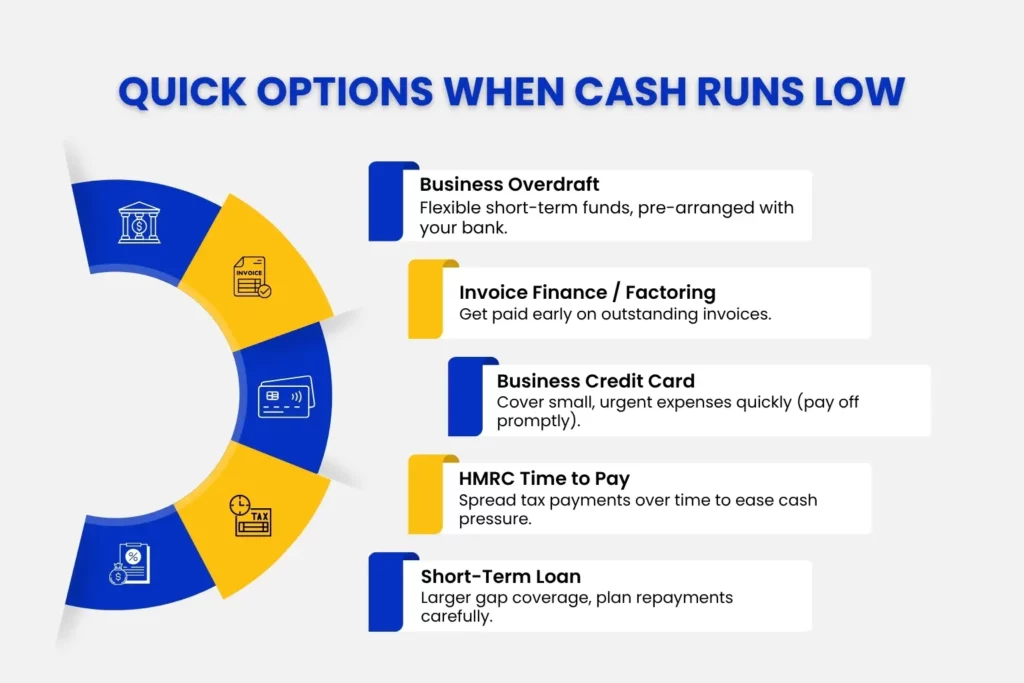

- Business overdraft. A pre-arranged business overdraft facility with your bank gives you flexibility for short-term gaps. It is worth setting this up before you need it.

- Invoice finance. If you have outstanding invoices, invoice finance or factoring allows you to release a percentage of the value immediately rather than waiting for the client to pay.

- Business credit card. For smaller, short-term costs, a business credit card can provide cover. Use with care and clear the balance as quickly as possible.

- HMRC Time to Pay. If a tax bill is contributing to the pressure, HMRC operates a Time to Pay scheme that allows you to spread the cost of arrears. Contact HMRC early rather than waiting until the deadline has passed.

- Short-term business loan. For larger gaps, a short-term loan may be appropriate. Compare rates carefully and make sure the repayment schedule is realistic given your cash flow.

These are tools for exceptional circumstances. The goal should always be to reduce reliance on external funding by building and maintaining a healthy reserve.

How Cash Flow Services & Management Accounts Support Your Cash Reserves

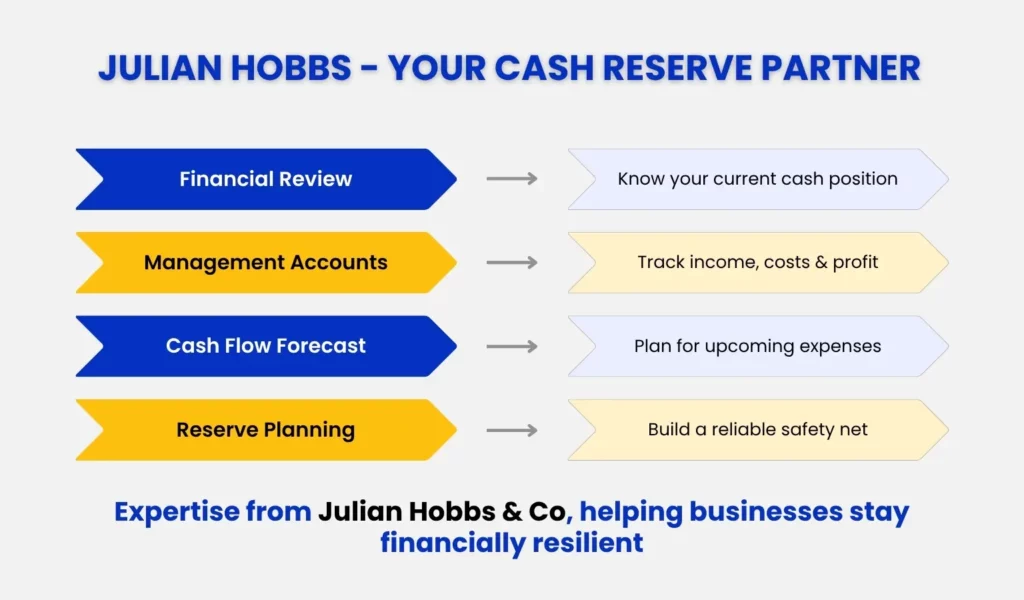

Building a cash reserve is not a one-off task. It requires ongoing visibility of your financial position.

Monthly management accounts give you a current picture of income, costs, and profit. They make it easy to see whether the business is generating enough surplus to contribute to reserves each month, and they flag early if cash is starting to tighten.

Cash flow forecasting goes a step further. It projects your expected income and outgoings over the coming weeks and months. A good forecast will highlight periods where your reserve is likely to be called upon, giving you time to prepare rather than react.

Together, these tools turn your cash reserve from a passive pot of money into an active part of how you manage the business.

How Julian Hobbs & Co Can Help

We help businesses and individuals across Welwyn, Hertfordshire and nearby regions build stronger financial foundations. Whether you need management accounts, cash flow forecasting, or straightforward advice on how much you should be holding in reserve, our team can help.

If you want to understand your current cash position and build a plan to improve it, book a call with our team. We will give you a clear picture and practical next steps.

People Also Ask:

What is a cash reserve account?

A cash reserve account is a dedicated savings account used to hold money set aside for emergencies or unexpected costs. It is kept separate from your day-to-day operating account and only drawn on when genuinely needed.

Is a cash reserve the same as a cash buffer?

Broadly yes. Both refer to money held aside to absorb financial shocks, but a reserve is physically separate from your operating cash needs. The terms are often used interchangeably.

How much should a small business keep in cash reserves?

Most advisers recommend two to three months of fixed costs for businesses with predictable income, and three to six months for those with variable or seasonal revenue.

Can a cash reserve account earn interest?

Yes. Business savings accounts and instant access deposit accounts pay interest on balances. Rates vary between providers. While the primary purpose of a reserve is accessibility rather than return, it makes sense to hold it somewhere that earns a reasonable rate.

What happens if a business has no cash reserves?

A business with no reserves is highly vulnerable. A slow month, a late-paying client, or an unexpected cost can quickly create a serious cash flow crisis. Without reserves, the only options are borrowing, cutting costs at short notice, or in the worst case, being unable to meet obligations to staff or suppliers.