Introduction

If you run a limited company, filing annual accounts is not optional. It is a legal requirement, and missing the deadline costs you money.

But beyond compliance, your annual accounts tell the story of your business. They show how it performed, what it owns, and what it owes. Done properly, they are a useful tool, not just a box to tick.

This guide covers everything you need to know about annual accounts for limited company, including what’s inside them, when to file them, and how to avoid the most common mistakes.

What Are Annual Accounts for a Limited Company?

Annual accounts are a formal set of financial statements that summarise a company’s performance over its financial year. Every private limited company in the UK must prepare them.

They are filed with Companies House, where they become part of the public record. This means that they are publicly available to be viewed. They are also used to support your Corporation Tax return, which is submitted separately to HMRC.

Annual accounts are sometimes called statutory accounts. The two terms mean the same thing.

Who Needs to Prepare Annual Accounts for a Private Limited Company?

Every private limited company registered in the UK must prepare and file annual accounts, regardless of size, turnover, or whether the company traded during the year. The level of details contained inside accounts varies according to size, however.

The filing requirement includes dormant companies. If your company is registered but not actively trading, you still need to file, though the accounts will be much simpler.

The responsibility sits with the company directors. It is the directors who are legally accountable for ensuring accounts are prepared accurately and filed on time.

What Do Annual Accounts Include?

The exact contents depend on the size of the company, but most limited companies will need to include the following.

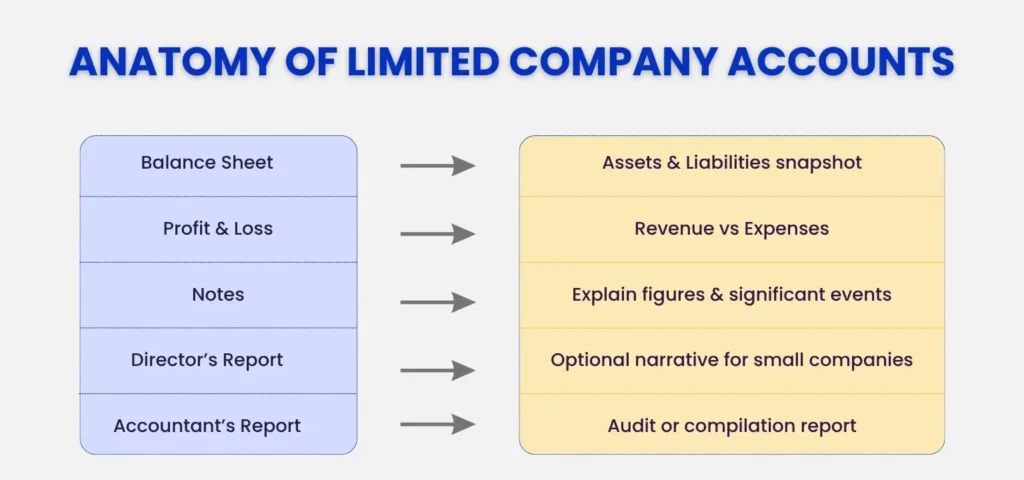

Balance Sheet

A snapshot of the company’s financial position at the end of the year. It shows what the company owns (assets) and what it owes (liabilities).

Profit and Loss Account

A summary of income and expenditure over the year, showing whether the company made a profit or a loss. Smaller companies may not be required to file this with Companies House but must still prepare it for shareholders and HMRC.

Notes to the Accounts

Supporting detail that explains the figures in the balance sheet and profit and loss. This includes accounting policies, breakdown of key figures, and any significant events that affected the numbers.

Director’s Report (if required)

A brief narrative from the directors summarising the company’s activities and performance. Micro and small companies are often exempt from filing this with Companies House, though it may still need to be prepared for shareholders. Your management accountant can take care of all this.

Accountant’s Report (if applicable)

Larger companies may require a formal audit. Smaller companies below the audit threshold can instead include a compilation report from their accountant, confirming the accounts have been prepared from the company’s records.

How to Prepare Annual Accounts for Private Limited Company

Preparation starts with accurate bookkeeping throughout the year. If your records are well maintained, producing the accounts at year end is straightforward. If they are not, it adds time and cost.

The process typically involves:

- Reconciling all bank accounts and ensuring transactions are correctly categorised

- Reviewing debtors and creditors to confirm what is owed to and by the company

- Calculating depreciation on fixed assets

- Making any necessary adjustments, such as accruals or prepayments

- Preparing the statutory financial statements in the correct format

- Obtaining director approval and signature before filing

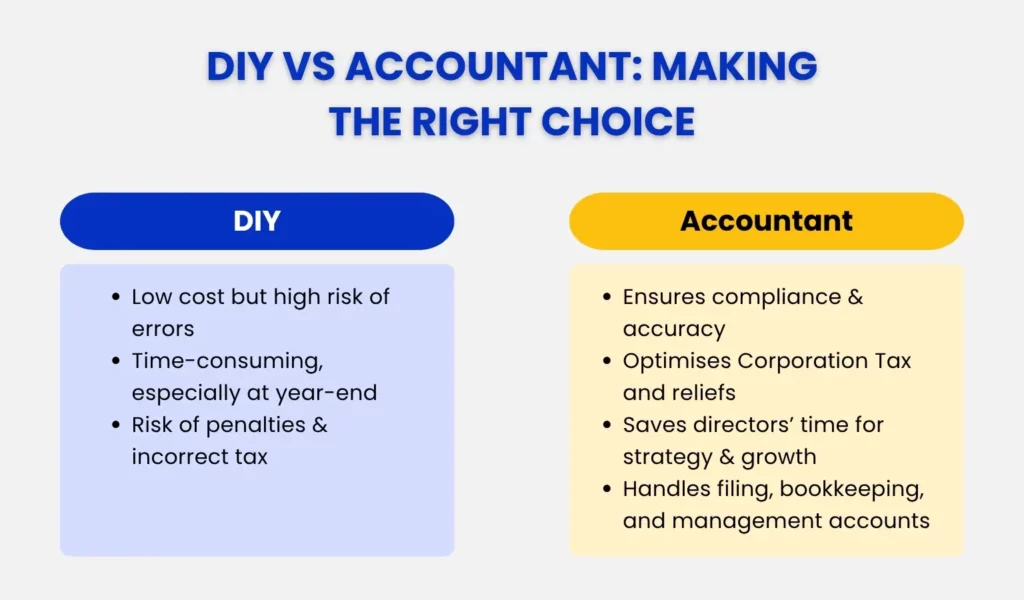

Most limited companies use an accountant for this process. It is possible to prepare and file accounts yourself, but the risk of errors is significant, and mistakes can lead to penalties or problems with your Corporation Tax position. Your accounts drive your tax liability, so it’s very important to have accurate annual accounts to provide a proper foundation for corporate tax planning.

How to File Annual Accounts for a Limited Company in the UK

Annual accounts are filed online through Companies House. Most accountants file directly through software linked to the Companies House system.

You will need your company’s authentication code to file. This is issued by Companies House when the company is incorporated. If you have lost it, you can request a new one, but allow time as it is sent by post.

When to File Annual Accounts (Deadlines Explained Clearly)

The filing deadline depends on whether the company is new or established.

- New companies must file their first accounts within 21 months of the date of incorporation.

- Existing companies must file within 9 months of their accounting reference date (the end of their financial year).

For example, if your financial year ends on 31 March 2025, your accounts must be filed with Companies House by 31 December 2025.

Note that the Corporation Tax return deadline is separate. You have 12 months from the end of the accounting period to file with HMRC, and Corporation Tax is due 9 months and one day after the year end.

What Happens If You Miss the Deadline?

Companies House applies automatic penalties for late filing. The fines increase the later you are.

- Up to one month late: £150

- One to three months late: £375

- Three to six months late: £750

- More than six months late: £1,500

These penalties double if you file late in two consecutive years. There is no appeal process for lateness unless there are genuinely exceptional circumstances.

Companies House can also take action to strike off a company that persistently fails to file. That would have serious consequences for the directors and any assets held in the company.

Do You Need an Accountant to Prepare and File Annual Accounts?

You are not legally required to use an accountant. Directors can prepare and file accounts themselves.

In practice, most limited companies use one. The accounts must comply with UK accounting standards, and errors can affect your tax position, your credit rating, and the public record of your company.

An accountant will also ensure the accounts are prepared in the most tax-efficient way, claiming all available reliefs and structuring the figures correctly for your Corporation Tax return.

Common Mistakes Businesses Make with Annual Accounts

- Leaving it too late. Annual accounts take time to prepare properly. Starting the process well before the deadline avoids rushed work and errors.

- Poor bookkeeping during the year. Unreconciled accounts, missing receipts, and mixed personal and business transactions all slow down the year-end process and increase the cost.

- Confusing the Companies House and HMRC deadlines. They are different. Missing either has consequences. Keep both dates clearly in your diary.

- Not reviewing the accounts before signing. Directors are legally responsible for the accounts. Read them carefully before approving.

- Assuming dormant means exempt. Dormant companies still need to file. The accounts are simpler, but the obligation remains.

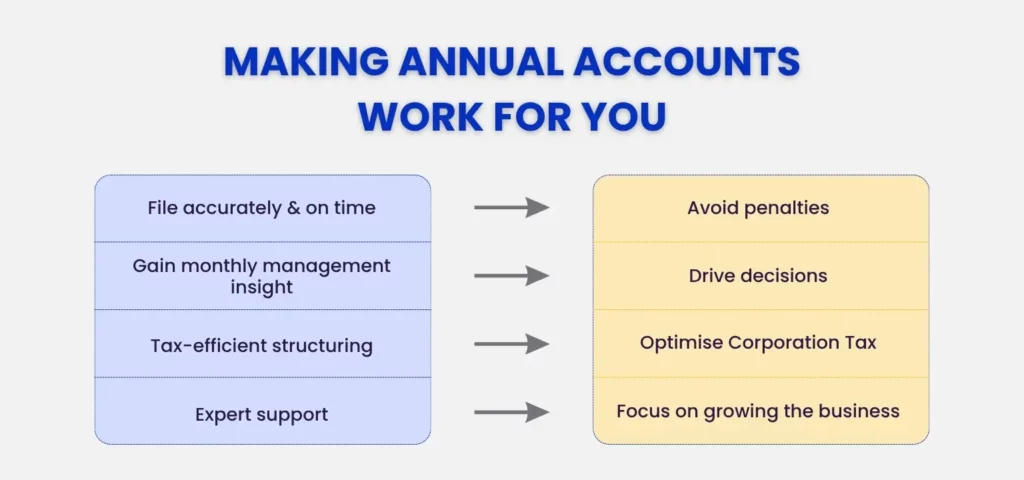

Why Annual Accounts Alone Are Not Enough for Growing Businesses

Annual accounts look backwards. They tell you what happened last year. By the time they are finalised and filed, the information can be nine months or more out of date.

If you are making decisions about hiring, investment, or growth, you need current financial information. That means monthly management accounts and cash flow forecasts, not just a once-a-year statutory snapshot.

Annual accounts satisfy your legal obligations. Management accounts help you run the business well. Both matter.

Key Takeaways

- Every private limited company must file annual accounts with Companies House, regardless of size or trading status

- The deadline is 9 months after your financial year end for existing companies

- Late filing penalties start at £150 and rise to £1,500, and double for consecutive late filings

- Directors are legally responsible for ensuring accounts are accurate and filed on time

- Annual accounts are a compliance requirement, not a substitute for regular financial management

How Julian Hobbs & Co Helps with Annual Accounts and Beyond

We prepare and file annual accounts for limited companies of all sizes all the time. We handle the process from start to finish: bookkeeping review, statutory accounts, Corporation Tax return, and Companies House filing.

We also provide monthly management accounts and cash flow support for businesses that want more than a once-a-year conversation with their accountant.

If your year end is approaching, or you want to get ahead of it, book a call with our team. We will make sure everything is in order and filed on time.

People Also Ask:

What are annual accounts for a limited company?

Annual accounts are a formal set of financial statements prepared at the end of each financial year. They include a balance sheet, profit and loss account, and supporting notes. Every private limited company in the UK must prepare and file them with Companies House.

When do you need to file annual accounts?

Existing companies must file within 9 months of their accounting reference date. New companies have up to 21 months from incorporation for their first set of accounts. Missing the deadline triggers automatic financial penalties.

How do you prepare annual accounts for a private limited company?

The process involves reconciling your records, reviewing debtors and creditors, calculating depreciation, making accounting adjustments, and preparing the statutory statements in the correct format. Most companies use an accountant to ensure accuracy and compliance.

Can I file annual accounts myself?

Yes, directors can prepare and file accounts without an accountant. However, the accounts must comply with UK accounting standards. Errors can affect your tax position as your accounts are used as the basis for the tax calculations. Most limited companies choose to use a professional.

What happens if I file annual accounts late?

Companies House applies automatic penalties starting at £150 for accounts up to one month late, rising to £1,500 for accounts more than six months late. Penalties double if you file late in two consecutive years.

Can Julian Hobbs & Co help with annual accounts and beyond?

Yes. We prepare and file annual accounts and Corporation Tax returns for limited companies across the UK. We also offer monthly management accounts, cash flow forecasting, and ongoing financial support for businesses that want to stay on top of their numbers throughout the year. Get in touch to find out how we can help.