Introduction

Most people know that savings interest is taxable. Fewer people know how much they can earn before tax actually kicks in. That is where the Personal Savings Allowance comes in.

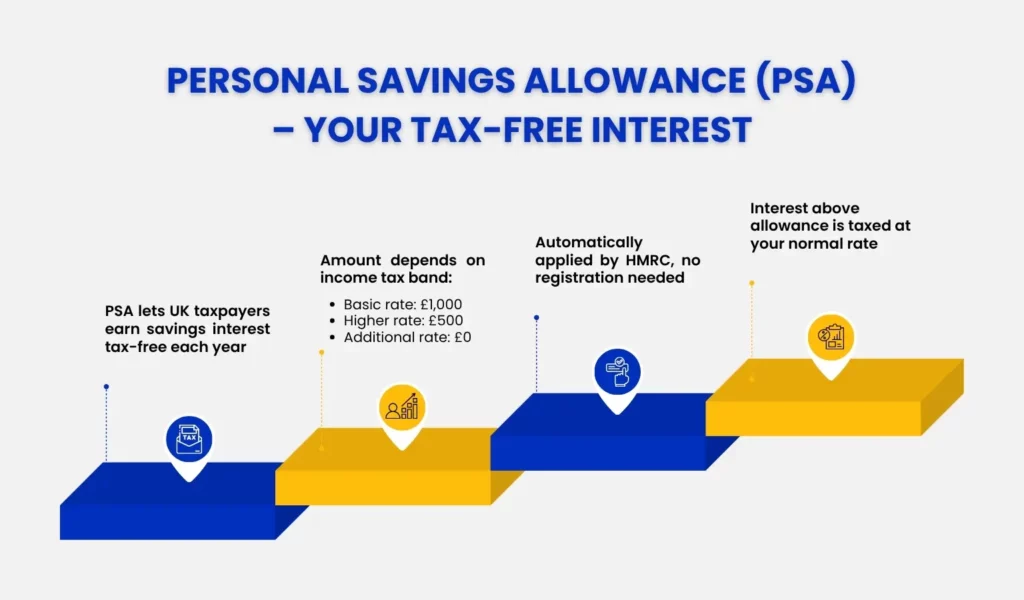

The Personal Savings Allowance, often shortened to PSA, lets most UK taxpayers earn a set amount of interest on their savings each year without paying tax on it. The amount you can earn tax-free depends on which income tax band you fall into.

But the PSA is only part of the picture. There is a lesser-known relief called the starting rate for savings that can allow some people to earn a significant amount of savings interest at 0%. When the two work together, the results can be surprisingly powerful.

This guide explains how both reliefs work, who can use them, and how to make the most of tax-free savings in the UK.

What is Personal Savings Allowance?

The Personal Savings Allowance is the amount of interest you can earn on your savings in a tax year before you have to pay income tax on it. It was introduced in April 2016 and applies to interest from bank accounts, building societies, credit unions, peer-to-peer lending, and most savings products outside of ISAs.

The PSA is not a separate account or product. It is simply an allowance that sits alongside your income. You do not need to apply for it or register anywhere. HMRC applies it automatically based on your income tax band.

Before 2016, banks deducted tax from savings interest at source. That changed with the introduction of the PSA. Banks now pay interest gross, and it is up to the taxpayer to declare it if they exceed the allowance.

How Does Personal Savings Allowance (PSA) Work?

The allowance is linked to your income tax band for the tax year in question. There are three tiers.

Basic rate taxpayers receive a PSA of £1,000. Higher rate taxpayers receive £500. Additional rate taxpayers, those earning above £125,140, receive no PSA at all.

So, if you are a basic rate taxpayer and you earn £900 in savings interest over the year, you pay no tax on it. If you earn £1,200, you pay tax on the £200 that exceeds your allowance. The rate you pay depends on your income tax band: 20% for basic rate, 40% for higher rate.

Interest from ISAs does not count towards the PSA. ISA interest is already tax-free, so it sits outside this calculation entirely.

One further point worth knowing: if your total income including savings interest exceeds £100,000, your Personal Allowance begins to be withdrawn. For every £2 of income above £100,000, you lose £1 of Personal Allowance. By £125,140, the full Personal Allowance is gone. Savings interest can contribute to pushing you into this range, which creates an effective tax rate of 60% on income within that band. If your earnings are close to £100,000, this is worth planning around carefully.

The Starting Rate for Savings: The Relief Most People Have Never Heard Of

Alongside the PSA, there is a separate relief called the starting rate for savings. It is one of the most underused reliefs in the UK tax system, and it can allow certain people to earn a substantial amount of savings interest completely free of tax.

The starting rate for savings is a 0% tax rate that applies to up to £5,000 of savings interest. It is available to people whose non-savings income, meaning earned income such as salary, pension, or self-employment profits, is low enough to leave room within this band.

Here is how it works. The starting rate band sits just above the Personal Allowance. For 2025/26, the Personal Allowance is £12,570. The starting rate band then covers the next £5,000 of income, from £12,570 up to £17,570.

If your non-savings income fills up this band, the starting rate is not available. But if your non-savings income is low, the unused portion of the £5,000 band can be filled by savings interest at 0%.

For every £1 of non-savings income above £12,570, the starting rate band reduces by £1. So someone with earned income of £15,570 has used £3,000 of the band through earned income, leaving £2,000 for savings interest at 0%.

A Worked Example: How Much Savings Interest Can Be Earned Tax-Free?

Consider someone who is semi-retired. They receive a part-time salary of £10,000 per year. Their non-savings income is therefore below the Personal Allowance of £12,570, so none of their earned income is taxable.

Because their non-savings income of £10,000 falls entirely within the Personal Allowance, the full £5,000 starting rate band remains available. Their savings interest can therefore be taxed at 0% up to £5,000.

On top of that, they also have their £1,000 PSA as a basic rate taxpayer.

The result is that this person can earn up to £6,000 of savings interest in the year completely free of tax: £5,000 covered by the starting rate band at 0%, plus £1,000 covered by the PSA.

At a savings rate of 4%, that means they could hold £150,000 in savings accounts and pay no tax whatsoever on the interest generated. That is a significant benefit, and most people in this position are simply unaware it exists.

This relief is particularly relevant for people who are winding down their working hours, taking a career break, or living primarily off savings while their earned income is low.

Personal Savings Allowance Freeze and Government Updates

Personal Savings Allowance Freeze: What Does it Mean?

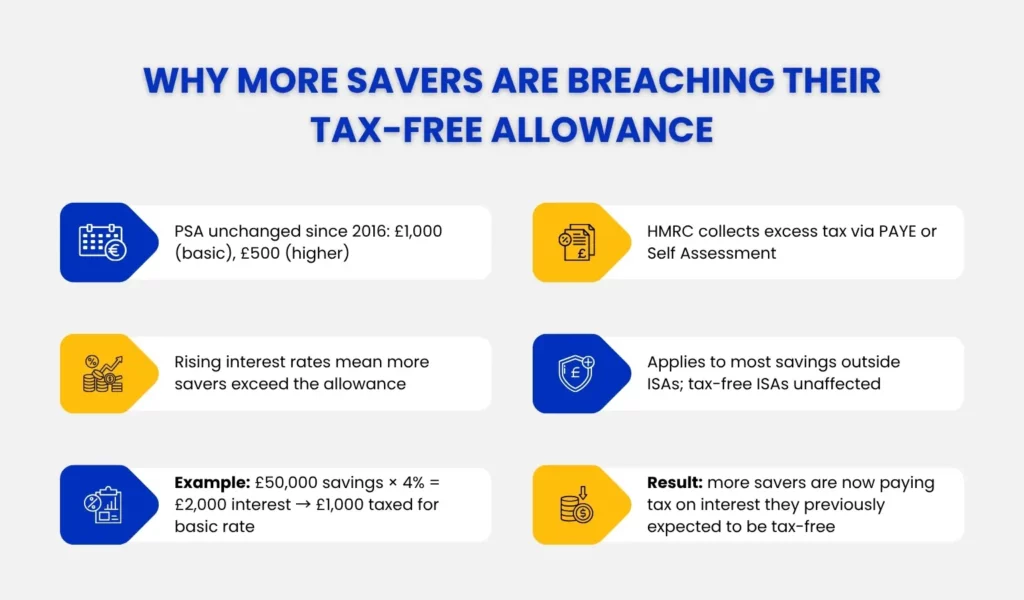

The PSA has not changed since it was introduced in 2016. Basic rate taxpayers still get £1,000 and higher rate taxpayers still get £500. In the meantime, savings interest rates have risen significantly.

In a low interest rate environment, it was relatively easy to stay within the allowance. With rates at historical lows, even a substantial savings pot would generate very little interest. That is no longer the case. Interest rates rose sharply after 2022, and many savers found themselves exceeding their PSA for the first time without making any changes to their behaviour.

A basic rate taxpayer with £50,000 in savings earning 4% interest would generate £2,000 in interest. That is twice the £1,000 allowance. Tax would be payable on the excess £1,000 at their marginal rate.

HMRC Personal Savings Allowance Tax Update

HMRC receives information from banks and building societies about the interest paid to customers. If your savings interest exceeds your PSA, HMRC will usually collect the tax owed by adjusting your tax code. For most employees and pensioners, this means the tax is collected through PAYE without any action required from you.

If you complete/file a Self Assessment tax return, you declare savings interest there instead. HMRC will calculate the tax owed as part of your overall bill.

With MTD for Income Tax set to change how many sole traders and landlords report income to HMRC from 2026, understanding your wider tax obligations is becoming increasingly important. Read our guide on MTD for Income Tax for Sole Traders & Landlords.

Types of Interest Covered by Personal Savings Allowance

The PSA covers most forms of savings interest, but not all. Knowing what counts is important so you do not accidentally underestimate your taxable interest.

Interest that counts towards the PSA includes interest from bank and building society accounts, credit unions, peer-to-peer lending platforms, and government or corporate bonds held outside an ISA.

Interest that does not count towards the PSA includes ISA interest, which is always tax-free, and dividends, which are covered by the separate dividend allowance.

Fixed rate bonds and notice accounts are included. If your bank account pays interest annually, the full amount is counted in the tax year it is credited. If interest is credited monthly, it all counts within that same tax year.

How Much Savings Do You Need Before Interest Is Taxed?

The answer depends on the interest rate you are earning and your tax band. Here are some examples based on a 4% interest rate.

A basic rate taxpayer with a £1,000 PSA would need savings of £25,000 at 4% to generate exactly £1,000 in interest. Anything above £25,000 would produce interest that exceeds the allowance.

A higher rate taxpayer with a £500 PSA would hit the limit with savings of just £12,500 at the same rate.

The practical takeaway is that if you have meaningful savings, it is worth checking whether you are likely to breach your allowance in the current tax year with Julian Hobbs’ tax planning services.

What Happens If You Exceed Your Personal Savings Allowance?

Exceeding your PSA does not mean you owe tax on all of your interest. You only pay tax on the amount above the allowance.

For most people in employment or receiving a pension, HMRC will adjust your tax code to collect the tax. You will see a change in your take-home pay or pension payment rather than receiving a bill directly.

If you complete a Self Assessment return, you include your total savings interest in the return and the tax is calculated there. The same applies to anyone with more complex finances, including company directors, landlords, and higher earners.

If HMRC does not have up-to-date information, you may receive a Simple Assessment letter asking you to pay tax owed. This is more common where interest income is significant or your tax affairs are not managed through PAYE.

Tax Free Savings Allowance vs. ISAs

The PSA and ISAs both allow you to shelter savings interest from tax, but they work in different ways.

The PSA is automatic. It applies to standard savings accounts and requires no action from you. You simply benefit from it up to the limit, and then pay tax on the excess.

An ISA works differently. You actively choose to put money into an ISA, and any interest earned inside it is completely tax-free with no upper limit. There is an annual ISA subscription limit of £20,000, but once money is inside an ISA, the interest it generates is never taxable.

For someone with a large savings pot, an ISA is often the more powerful option. If you have savings that generate more interest than your PSA covers, moving some or all of those savings into a cash ISA removes the tax problem entirely.

The two tools can also work together. You can hold savings in both an ISA and a standard account, using your PSA for interest earned outside the ISA, while keeping larger balances inside the ISA where the interest always remains tax-free.

Want to explore more tax-efficient saving options beyond ISAs? Read our complete guide to Tax Free Savings Accounts in the UK.

How Julian Hobbs & Co. Can Help

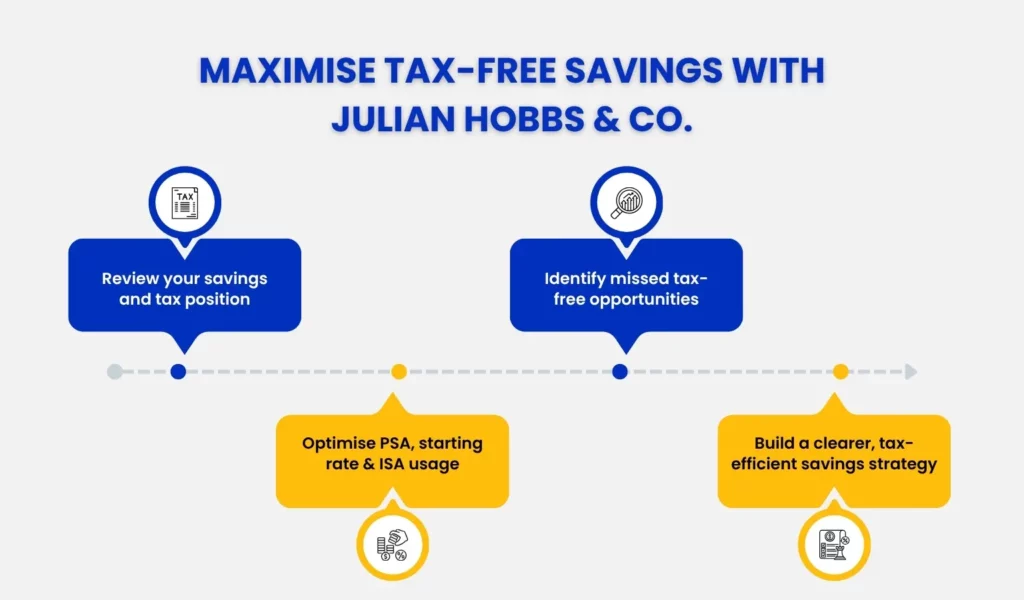

Whether you are approaching your PSA limit or have already exceeded it, getting the right advice can save you money and stress.

At Julian Hobbs & Co., we help individuals review their savings, understand their tax position, and plan in a way that uses available allowances effectively. We look at the full picture: income, savings, dividends, and reliefs together, so nothing gets missed.

If you want to understand how much tax you are paying on your savings and whether there is a more efficient way to structure things, book a call with our team. We will explain everything clearly and help you make the most of what is available to you.

As your savings, investments, or business interests grow, having the right accountant becomes increasingly important. Explore the 5 Blind Spots Scaling Welwyn Business Owners Overlook When Choosing an Accountant.

Conclusion

The Personal Savings Allowance is a useful and often overlooked benefit. For basic rate taxpayers especially, it means a meaningful amount of savings interest can be earned completely free of tax.

When you add in the starting rate for savings, the picture becomes even more interesting. For people with low earned income, the combination of the Personal Allowance, the starting rate band, and the PSA can stack up to £6,000 of savings interest at 0%. That is a benefit well worth knowing about.

But with the PSA frozen since 2016 and savings rates significantly higher than they were a few years ago, more people are now exceeding the limit without realising it. If your savings have grown or your tax band has changed, it is worth reviewing your position.

HMRC has also increased scrutiny around untaxed savings interest in recent years. Read our guide on HMRC Savings Account Tax Warnings and what UK savers should know.

People Also Ask:

What is the Personal Savings Allowance?

It is the amount of savings interest you can earn each tax year without paying income tax on it. Basic rate taxpayers receive £1,000, higher rate taxpayers receive £500, and additional rate taxpayers receive nothing.

Who qualifies for the Personal Savings Allowance in the UK?

Most UK taxpayers qualify. Basic rate and higher rate taxpayers both receive a PSA. Additional rate taxpayers, those earning above £125,140, do not receive any allowance.

How do I calculate if I have exceeded my Personal Savings Allowance?

Add up all interest earned from savings accounts, bonds, and other eligible sources outside of ISAs in the tax year. If the total exceeds your PSA for your tax band, you have exceeded it.

Can savings interest push me into a higher tax bracket?

Yes. Savings interest counts as income. If your total income including savings interest pushes you above £50,270, you move into the higher rate band. That also reduces your PSA from £1,000 to £500. If it pushes you above £100,000, your Personal Allowance begins to be withdrawn, creating an effective tax rate of 60% on that portion of income.

Does the Personal Savings Allowance apply to foreign savings?

Yes, in most cases. If you are a UK taxpayer, interest from overseas savings accounts is generally taxable in the UK and counts towards your PSA in the same way as UK interest. You may also need to declare it on a Self Assessment return.

What happens if I exceed my Personal Savings Allowance?

You pay income tax on the amount of interest above your allowance. HMRC usually collects this by adjusting your tax code or through your Self Assessment return. You do not need to contact HMRC yourself in most cases, but it is worth checking your tax code each year.

What is the starting rate for savings and who can use it?

The starting rate for savings is a 0% tax rate on up to £5,000 of savings interest. It is available to people whose non-savings income is low enough to fall below £17,570. For every £1 of non-savings income above the Personal Allowance of £12,570, the starting rate band reduces by £1. People with low earned income, such as part-time workers or those in semi-retirement, are most likely to benefit.

How can Julian Hobbs & Co. help me manage my Personal Savings Allowance?

We review your full income picture, including savings interest, dividends, and other sources, to make sure you are using your allowances effectively and not paying more tax than necessary. Get in touch to book a call with our team.