A Quick Brief

Since the readers of this particular blog are mostly self employed professionals, let us understand with an example of “James, a graphic designer based in Hertfordshire” – the concept of payment on account.

James had set his business back in early 2024 – ensuring he was organised at all times, sent his invoices on time, and was ready with his self-assessment when Jan 2025 rolled around.

His tax bill came to £3200, and he transferred the money across.

But, instead of taking £3200, HMRC had taken £4,800.

Panic set in. He rang his accountant, hoping for an error on the authority’s end. The answer? Payment on account – HMRC’s system of spreading your tax burden over the course of the year towards your upcoming tax bill, based on the previous year’s tax liability.

This guide is written for every James out there – freelancers, sole traders, landlords and side-hustlers who deserve a plain English explanation of how payment on account actually works.

You’ll also come to know the deadlines, calculation process and how to reduce your liability – side by side managing your cash flow.

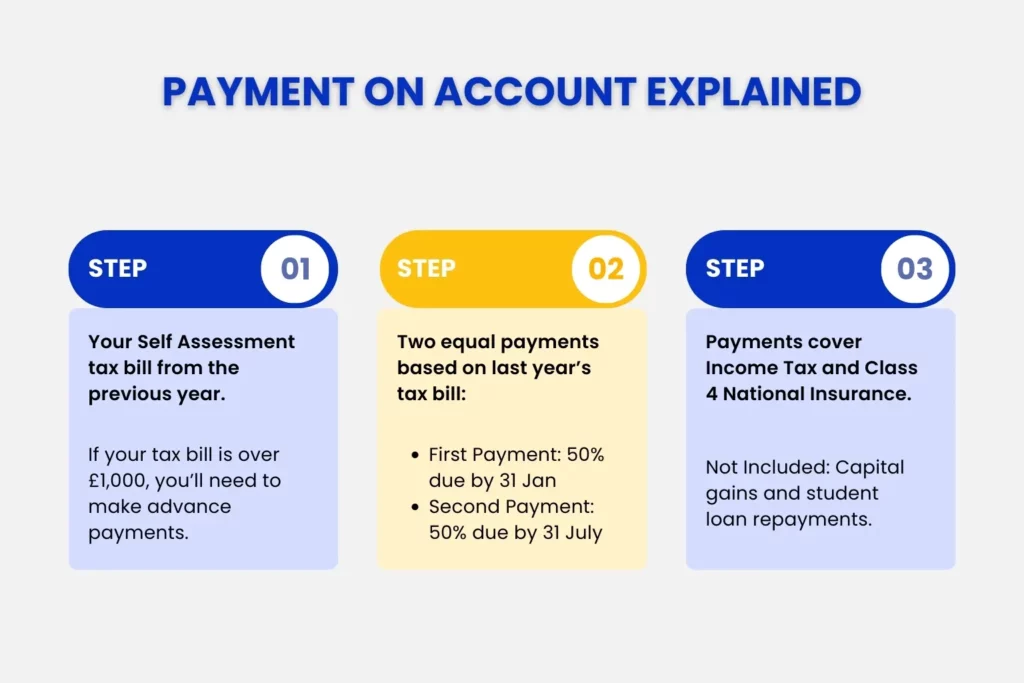

What Is Payment on Account? (HMRC Rules Explained)

Payment on Account is HMRC’s system of collecting tax in advance. It involves making two advance payments toward next year’s bill based on the previous year’s tax liability.

Let’s take the example of James. In 2025, his bill came to £ 3200. Since this is greater than the £1,000 threshold, and assuming around 80% of his tax isn’t paid at source (via PAYE), he now needs to make advance payments. The first payment on account will be due on Jan 31, 2026, and the second on July 31st, 2026 – therefore, £1600 is to be paid in Jan and the remaining £1600 in July.

Remember, these payments cover your Income Tax and, if self-employed, your Class 4 National Insurance. They do not include capital gains and student loan repayments.

So, if James made a capital gain of £10,000 from selling an asset in 2025, this would not be included in his payments on account for 2026. Nor would his student loan repayments, if applicable.

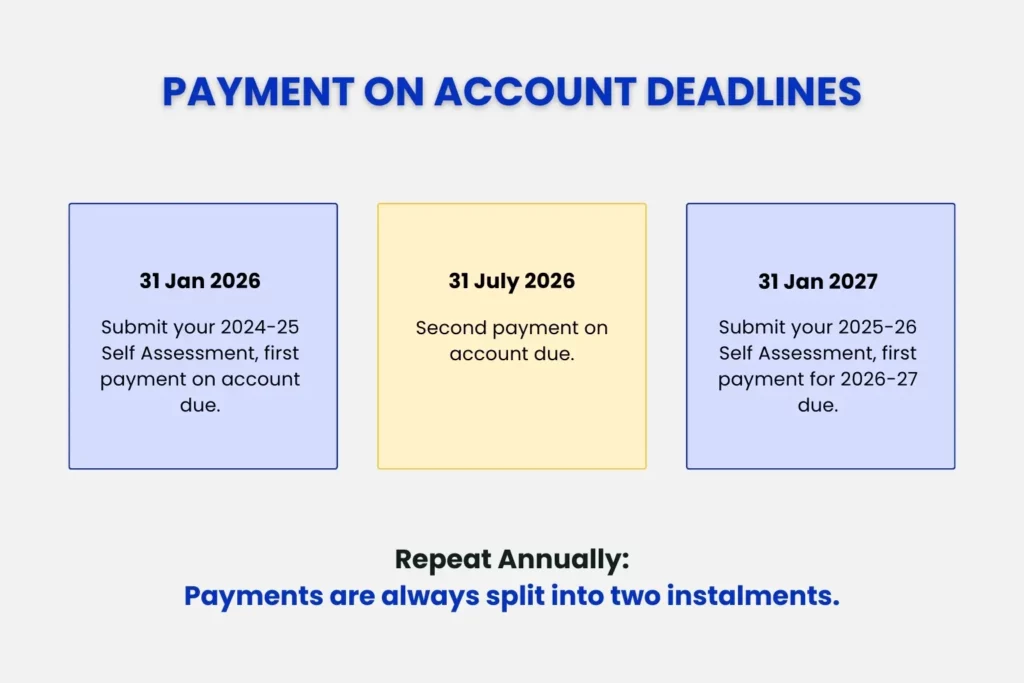

Self Assessment Payment on Account Deadline 2026 Calendar

Follow the pattern below and get the dates fixed in your head right now.

- 31 January 2026: By midnight on this date, you must submit your 2024-25 self assessment tax return, pay any balancing payment owed for 2024-25 and make your first payment on account towards the 2025-26 tax year.

- 31 July 2026: You’ll be making your second payment on account for 2025-26. You won’t be having any return to file, no balancing payment – just the second instalment – clean and straightforward.

- 31 January 2027: The cycle continues. You will be submitting your 2025-26 self assessment tax return, settling any balancing payment and starting with the first instalment of 2026-27 all over again.

The pattern never really changes. What does change is the amount. In James case, he’d have to pay:

- First Payment on Account – January 31, 2026 (amount owed £1600)

- Second Payment on Accounting – July 31, 2026 (amount owed £1600)

Is Payment on Account Compulsory for Self Assessment?

Yes, Payment on Account is compulsory for most self-assessed individuals, with two specific exceptions.

- You are not required to make payments on account if your previous Self Assessment tax bill was under £1,000.

- If at least 80% of the tax you owed was already collected at source (typically through PAYE)

If James, let’s say, has taken a three-day-a-week in-house role at an agency with a proper employment contract & PAYE system, with his salary being around £31,570. Then, the tax deducted at source (PAYE) would be

| Income Source | Gross Income | Tax Deducted |

| Employment (PAYE) | £31,570 | £3,800 collected at source |

| Self-employment (James) | – | £600 owed via Self Assessment (£1600 – £1000) |

| Total tax liability | – | £4,400 |

This £3,800 (out of the £4,400 total liability) roughly accounts for 86% of tax already collected at source (PAYE). Since it’s more than 80%, James now does not need to make a payment on account for the 2025-26 tax year. He simply has to pay the balance of £600 by 31st January, 2026 midnights. No July instalments – no advance payment.

How Do I Calculate My Payments on Account Amount?

Carrying forward the same figures and examples, here’s how you can calculate your Payment on Account:

For James, this would be paying 50% of the previous year’s self assessment liability of £3,200 into two payments

- First payment on Account: £1,600 (due 31 January 2026)

- Second payment on account: £1,600 (due 31 July 2026)

- Total paid in advance: £3,200

Now, suppose his actual liability came at £3,800 ( far from the total advanced payment made – £3,200). He will now owe a balancing payment of £600 in January of the following year.

In the other case, if his actual bill turns out to be only £2,700, HMRC will then owe him a £ 500 refund the following year (January 31st, 2027).

The maths isnt’ that complicated, once you’re used to it. But the cash flow implications are significant.

Setting aside around 25–30% of your net income into a separate account specifically for tax – is one of the most straightforward habits you can build to protect yourself.

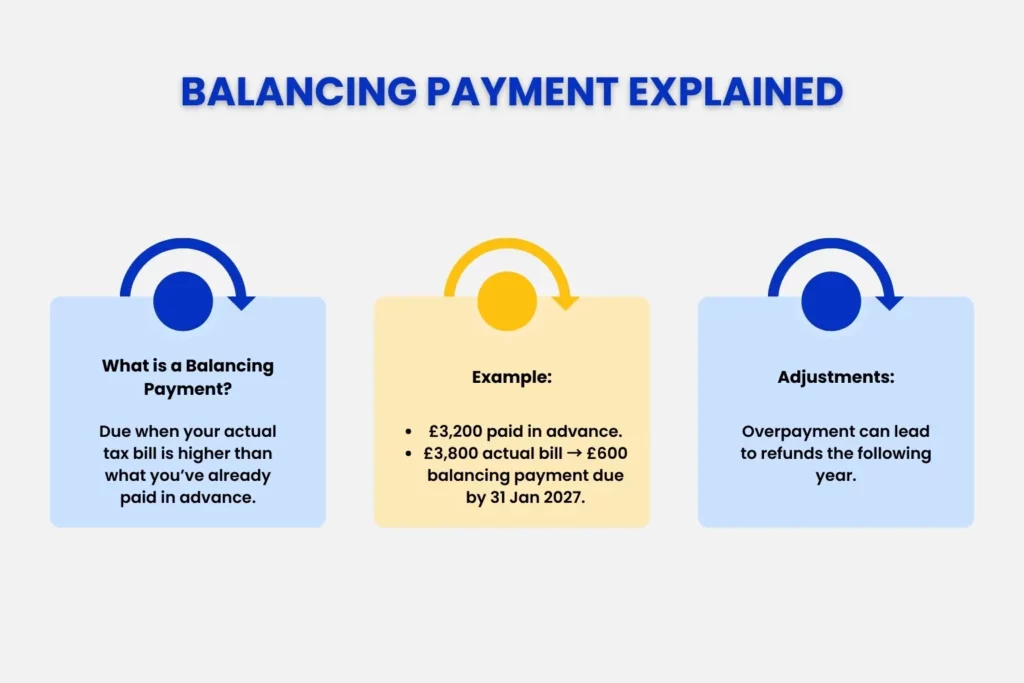

What Is a Balancing Payment – And 2026 Schedule

A balancing payment is the extra payment you owe when your actual tax bill turns out to be higher than what you’ve already paid through two instalments. It is due by January 31st of the following year.

Going back to James, for the 2025-26 tax year, when his total amount paid in advance was £3,200 (£1600 paid by 31st Jan & £1600 by July). However, the real liability came at £3800. Now, he owes a £600 balancing payment + first payment on account by 31 January 2027.

- Balancing payment for 2025-26 = £600

- First payment on account for 2026-27 (50% of £3800) = £1900

- Total due 31 January 2027 = £2,500

- Second payment on account due by July 2027 = £1900

Reduce Payment on Account 2026 (SA303 Guide)

If you know or believe that your current tax bill is going to be lower than last year’s, you can contact HMRC to reduce payment on account. This can be, maybe because you have gone back to employment or had a decline in trading trend. Either way, if you make a full payment on last year’s earnings, it means you are overpaying unnecessarily.

In such cases, you can apply to reduce your payment on account – either online or by submitting the SA303 form by post.

Here’s how to reduce your payments on account online:

- Log in to your HMRC Self Assessment account

- Select ‘View your latest Self Assessment return’

- Choose ‘Reduce payments on account’

- Enter the new, lower amount you expect to owe for the current tax year

- HMRC will recalculate your instalments accordingly.

How to use SA303 by post:

This is a single one-page document, where you fill in your UTR, the tax year in question and your estimate amount, and send it to your tax office before the payment deadline.

Reminder- A word of caution

If you underestimate your income, and your actual bill comes in higher than what you’ve declared, HMRC will charge interest on the difference.

The honest, practical approach is to only reduce payment account if you have a concrete, reasonable basis. If you’re unsure, then make the payment on account based on your previous year’s tax liability. Any difference – maybe you have paid too much, will be refunded by HMRC 100%.

Who Is Exempt from Payments on Account + Late Penalties

As covered earlier, the two routes to exemptions are

- You are not required to make payments on account if your previous Self Assessment tax bill was under £1,000.

- If at least 80% of the tax you owed was already collected at source (typically through PAYE)

As for the penalties, HMRC starts charging interest the day after the missed deadline. There’s no warning, no grace period.

As of 2026, the late payment interest rate sits at the Bank of England base rate plus 2.5 percentage points. This applies to both the balancing payment and the payments on account from the moment they fall overdue

- If James hasn’t paid by 2nd March, 2026 – 30 days after the January deadline – HMRC applies 5% penalty on the unpaid amount (£1,600 × 5% = £80 penalty).

- If the payment still remains outstanding even after 6 months from the original deadline – additional 5% penalty is charged.

- Likewise, if it reaches January 2027 – after 12 months – a third 5% penalty hits – bringing the total penalty to £240, plus all interest charges on all late payments from the due date until paid.

So, what if you genuinely cannot pay:

You then have to contact HMRC to apply for a Time to Pay Agreement. This can allow taxpayers to spread what they owe across an agreed period in monthly instalments. Interest still applies, but the 5% penalty can be avoided.

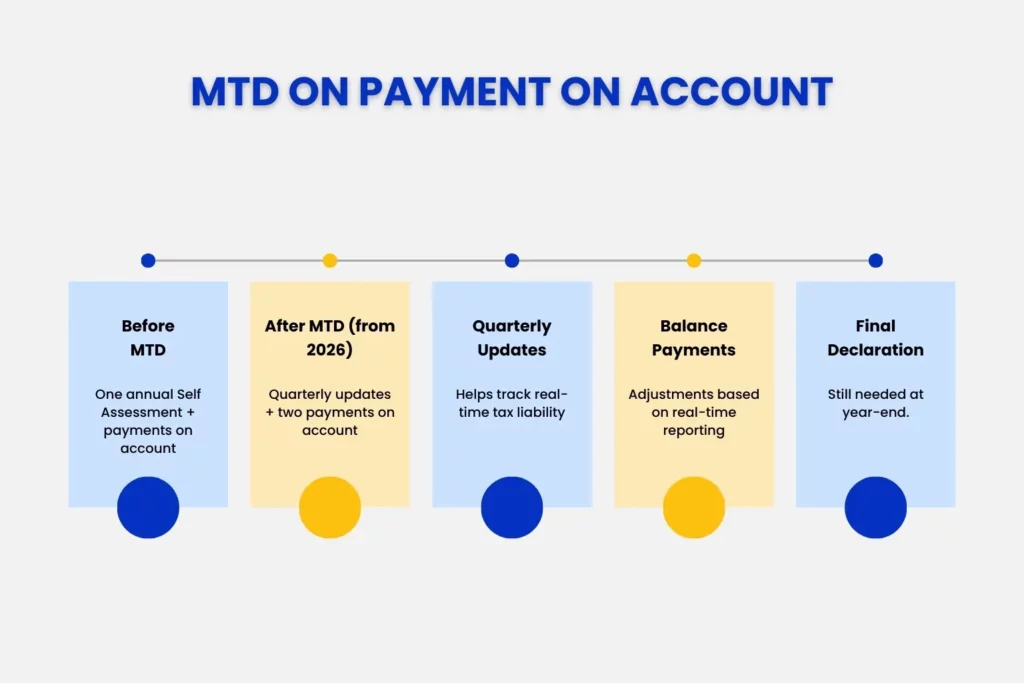

How MTD for Income Tax Affects Payments on Account from April 2026

MTD for Income Tax Self Assessment is a new HMRC system that comes into effect from April 2026 for sole traders & landlords with combined income over £50,00.

Under this, instead of submitting one annual self assessment return, you’ll be using HMRC-compatible software to send 4 quarterly updates plus a final end-of-year declaration.

The payment on account system does not disappear under MTD. You still have to make two advance payments and a balancing payment. But the quarterly reporting creates something valuable that many self employed people lack: an up-to-date, real-time picture of your tax liability throughout the year.

You’ll get a much clearer sense of whether your payments are roughly right, whether a reduction via SA303 is justified, or whether you should be putting more aside.

Conclusion

Payment on Account trips people not because it’s complex, but because it arrives unexpectedly. James’ story is repeated by thousands of self employed people every Jan, even if everything they’ve done is right.

The system itself is straightforward – two instalments – each equalling 50% of last year’s bill. Deadlines are on 31st January and 31st July. A balancing payment if the actual income turned out higher, a refund if lower. And the SA303 form or online claim to reduce payment on account.

James now feels more control over his taxes because he understands this system and can plan proactively.

How Julian Hobbs Helps with Payments on Account & MTD

Julian Hobbs & Co. specialises in helping sole traders, landlords and small business owners across Hertfordshire with tax planning, self assessment, payment on account and MTD compliance. Let us help you so you can fully focus on growing your business, while we handle your accounting & tax needs – efficiently and jargon-free.

People Also Ask:

Define payment on account in simple terms.

If you’re self-employed or owe tax through self-assessment, HMRC will ask you to make two advance payments each year. These payments are usually based on your tax bill from the previous year and are due by 31st January and 31st July.

Is payment on account compulsory?

Yes, with exemptions

– You are not required to make a payment on account if your previous self assessment tax bill was under £1,000.

– If at least 80% of the tax you owed was already collected at source (typically through PAYE)

Otherwise, it is compulsory for most self-assessed individuals, sole traders, landlords and contractors.

How do I calculate my payments on account amount?

Payment on account is calculated on your previous year’s tax bill. If your tax return for the previous year is at or above £1000, you are liable to make 2 instalments. First – being on 31st Jan, and second payment on account at 31st July in the same tax year.

When must I make payments on account in 2026?

After assessing your previous year’s tax bill, and crossing the £1000 threshold(i.e., after deductions from PAYE), and if most of your income isn’t taxed at source, you will be required to make payments on account in two instalments.

– First payment on account – 31st January 2026

– Second payment on account – 31st July, 2026

What is a balancing payment in self-assessment?

A balancing payment is the extra payment you owe when your actual tax bill turns out to be higher than what you’ve already paid through two instalments. It is due by January 31st of the following year.

How to reduce payment on account with HMRC using SA303?

If your income has decreased significantly or if you believe your tax bill for the year will be lower than the previous year, you can reduce your payments on account using the SA303 form.

This form allows you to request HMRC to lower the advance payments. After submitting the form, HMRC will review your situation and, if accepted, your payments on account for the following year will be adjusted.