As a builder or contractor in Hertfordshire, you know that your business doesn’t operate like a standard retail shop or a simple service consultancy. You deal with long lead times, fluctuating material costs, and the constant juggle of subcontractors. Whether you are working on high-end residential builds in Berkhamsted or commercial refits in Watford, you are operating in a high-stakes, high-cost environment. Yet, many construction firms are still trying to manage their empires using basic, “off-the-shelf” financial reports that fail to capture the complexity of the trade.

If you are looking at a standard Profit & Loss (P&L) statement once a quarter and thinking you have a handle on your business, you might be building on shaky foundations. There’s a real difference between financial accounting and management accounting, and most builders are only getting half of it. To truly scale, protect your margins, and navigate the unique pressures of the Home Counties construction market, you need management accounts for construction companies that are tailored to the specific way you work.

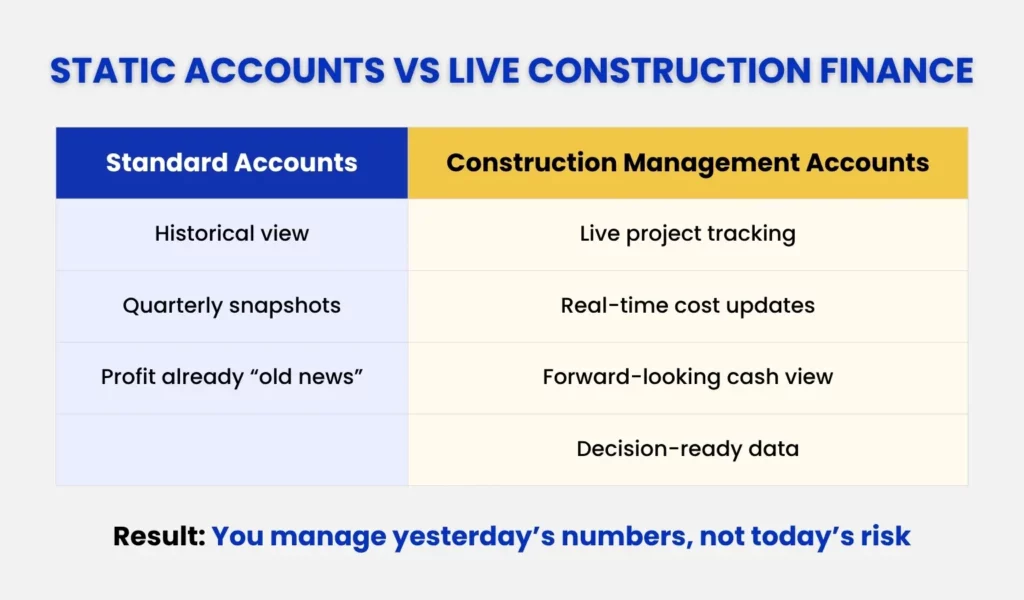

Why Standard Management Accounts Don’t Work for Construction

You’ve probably seen it before: your bank balance looks healthy, you’ve just finished a big project in St Albans, and your accountant sends over a standard P&L. It says you’re in the black. But then, a month later, you’re hit with a massive VAT bill, three subcontractor invoices you forgot were pending, and you realise a retention payment is stuck for another twelve months.

Standard accounts look backwards. They tell you what happened, but they don’t tell you what is happening right now on-site. In construction, the timing of when you spend money versus when you get paid is often out of sync. Without specific adjustments for things like Work in Progress (WIP) or CIS, a standard report can give you a dangerously false sense of security.

For a Hertfordshire builder, this “lag” in information can be fatal. In an area where land values are high and client expectations are even higher, a single project running over budget can wipe out the profits of three successful ones. You need real-time data to pivot before a project becomes a “vampire job” that sucks your resources dry. Standard accounting often ignores the reality of project-based billing, where a large deposit can look like profit, but it’s actually a liability for work yet to be done.

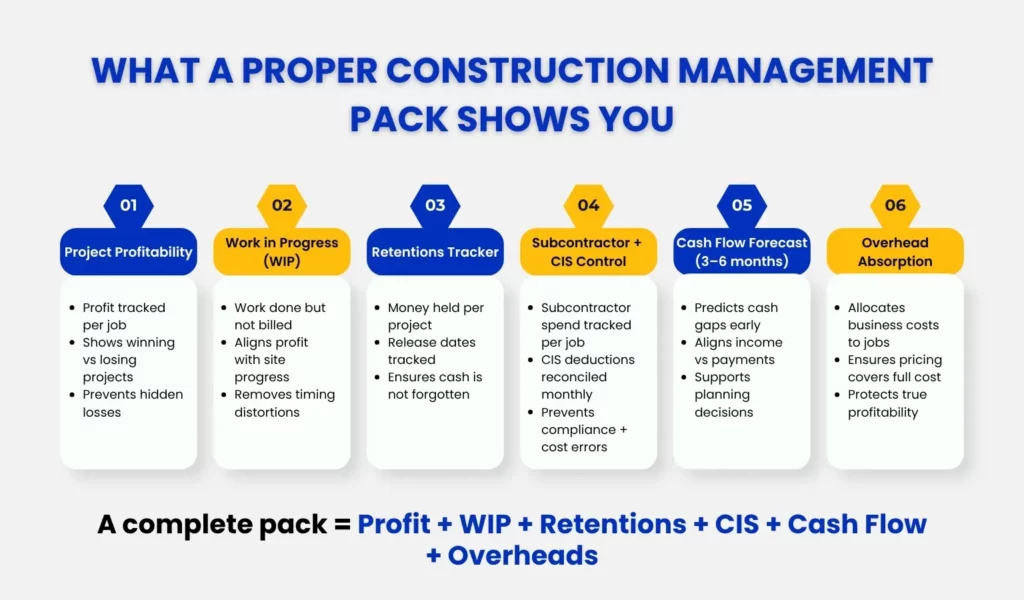

The 6 Things Every Construction Management Accounts Pack Must Include

To get a real grip on your numbers, your monthly pack needs to go deeper than just “money in vs. money out”. Here are the six pillars of effective management accounts for construction companies.

1. Project-Level Profit & Loss (Not Just Overall P&L)

You might be profitable as a company, but do you know which specific jobs are making you money and which are losing it? You need to see the P&L for each individual project. This allows you to identify if your site manager in Hertford is overspending on materials or if your pricing for domestic extensions is consistently too low.

Project-level reporting changes the way you bid. If your data analysis shows that you are losing money on your kitchen fits; however, you are excelling at loft conversions, you can tailor your sales approach accordingly. Failing to acquire this detailed analysis, you are just playing the odds when you send a quote. This will also ensure that you keep your team in check; if one site is always on target, whilst the other is always over budget, you will be able to identify the operational reason why.

2. Work in Progress (WIP) — Correctly Valued Each Month

This is the “secret sauce” of construction accounting. WIP accounts for the work you have done but haven’t yet invoiced, or money you’ve received for work not yet completed. Without a monthly WIP valuation, your profit figures will swing wildly every month, making it impossible to plan for the future.

Imagine you’ve spent £20,000 on materials and labour for a site in Berkhamsted this month, but you won’t be able to bill the client until the next milestone is hit in three weeks. A standard P&L would show a £20,000 loss this month. Management accounts adjust for this by recognising £20,000 is an asset (Work in Progress), giving you a true reflection of your monthly performance. This “accrual” method is the only way to see if you are actually making money on the work you are physically doing today.

3. Retentions — What’s Owed, When It’s Due, and Whether It’s At Risk

Retentions can represent your entire profit margin on a job. You need a clear report showing exactly how much is being held back, when the defects liability period ends, and when you can legally chase that cash.

If you aren’t tracking this in your monthly management accounts, it’s easy for thousands of pounds to simply slip through the cracks. In Hertfordshire’s competitive market, leaving 5% of your contract value on the table because you forgot to claim it at the end of the year is an expensive mistake you can’t afford to make. It’s also one of the quieter ways late payment problems take root in construction businesses — money that was always yours, just not yet collected. Your management pack should include a “Retention Ageing Report”, so you never lose sight of money that is rightfully yours.

4. Subcontractor Costs and CIS Position

Managing subcontractors is a full-time job in itself. Your management accounts should clearly show your Construction Industry Scheme (CIS) position. Are you deducting the right amounts? Are your CIS returns reconciled? This section ensures you stay on the right side of HMRC while keeping a firm eye on your highest variable cost.

You also need to track “cost to complete” for your subcontractors. If you’ve budgeted £10,000 for electrical work but the sparky is already at £9,000 and the first fix isn’t finished, your management accounts should flag that variance immediately. This allows you to have the difficult conversations with subcontractors early, rather than waiting for a surprise invoice at the end of the project.

5. Cash Flow Forecast — Not Just a Snapshot, But a Forward View

In construction, cash is your lifeblood. A snapshot of your bank balance today is useless if you have a £50k payroll run next Friday and no valuations being paid until the following month. You need a rolling cash flow forecast that looks at least 3-6 months ahead.

A robust forecast allows you to see the “valleys” in your cash reserves before you reach them. This allows you to find a better deal with suppliers, set up a temporary overdraft or press for the valuation payment to be made soon. It also gives you an idea whether you can afford to take that next big contract in St Albans, as growth can be expensive in the short term.

6. Overhead Absorption Rate — Are You Pricing to Cover Your Cost?

Are your project margins high enough to cover your office rent, your yard, your insurance, and your admin staff? By calculating an overhead absorption rate, you can ensure that every quote you send out contributes its fair share to the running of the business, not just the materials and labor on that specific site.

Many builders make the mistake of only pricing for the “sharp end” of the job—the bricks and the bodies on site. But if your overheads aren’t being absorbed by your projects, you aren’t actually making a net profit. Your management accounts should reveal exactly how much each project needs to contribute to your “back office” costs to ensure the whole company remains sustainable.

If juggling project-level P&Ls, retentions, WIP and CIS reconciliation on top of running the business is starting to feel like a second job, that’s exactly what our construction accountants are built for — finance support shaped around how Hertfordshire builders actually work.

The Numbers That Matter Most to a Hertfordshire Builder

Your local context matters. You are operating in a high-cost area with a competitive labor market. Your management accounts should help you track your “Gross Margin”—the percentage of revenue left after direct project costs.

The healthy margin in the UK is range-specific, but most builders use 15% to 25%. Once you understand yours, you can compare it with your competitors and see how to adjust your bid strategy. So, if margins are deteriorating, is it due to material costs rising in the UK, or is it due to a decline in labour productivity? Your management accounts will tell you.

Furthermore, you should be tracking your Variation Rate. How much of your profit is coming from the original contract versus variations agreed upon during the build? If you aren’t capturing and billing for every extra tile or hour of labour in St Albans, you are essentially working for free.

Best Accounting Software for Construction Management — What Actually Works for UK Builders

You need tools that talk to each other. Gone are the days of spreadsheets that only one person knows how to update. The best accounting software for construction management in the UK usually involves a core system like Xero, often bolstered by construction-specific “add-ons”.

Xero is widely considered the best accounting software for construction management due to its ease of use and built-in CIS features. It can automate much of the headache involved in subcontractor payments and domestic reverse charge VAT. For larger firms, integrating Xero with project management software allows you to see real-time costs against your budget.

Using the best accounting software for construction management means your data is live. You can check your project status on your phone while standing on a muddy site in Hatfield, rather than waiting for a paper report at the end of the month. It also allows your accountant to provide proactive advice rather than just filing historical returns.

A Real Example — “James” From Hertford

Consider “James”, a contractor based in Hertford. James was busy, his van was always on the road, and his team was growing. However, he always felt “cash poor”. He was winning big contracts but constantly struggling to pay his suppliers on time.

When we looked at his management accounts, we realised he wasn’t tracking his retentions properly—over £40,000 was sitting in old projects that he had simply forgotten to claim. We also found that two of his “regular” projects were actually running at a loss because he hadn’t updated his material costs in eighteen months. With the right management pack, James turned his cash flow around in just one quarter. He stopped taking on low-margin work and focused on the projects that his data proved were profitable.

Want to see what a clean monthly pack — the kind that turned James’s cash flow around — actually looks like? Our management accounts example guide breaks down exactly what a good report should include.

The Most Common Management Accounting Mistakes in Construction Businesses

- Ignoring WIP: Reporting profit based on bank balance rather than work completed. This leads to “lifestyle creep” during months with high deposits, followed by a cash crisis when the work actually needs to be done.

- Mixing Personal and Business Expenses: Making it impossible to see the true health of the company. If you’re paying for your family car through the business account without proper allocation, your project margins are lies.

- Poor Record Keeping: Not capturing site variations, which leads to “scope creep”, where you do extra work for free.

- Forgetting Retentions: Treating retentions as a “bonus” if they arrive rather than earned income that needs chasing.

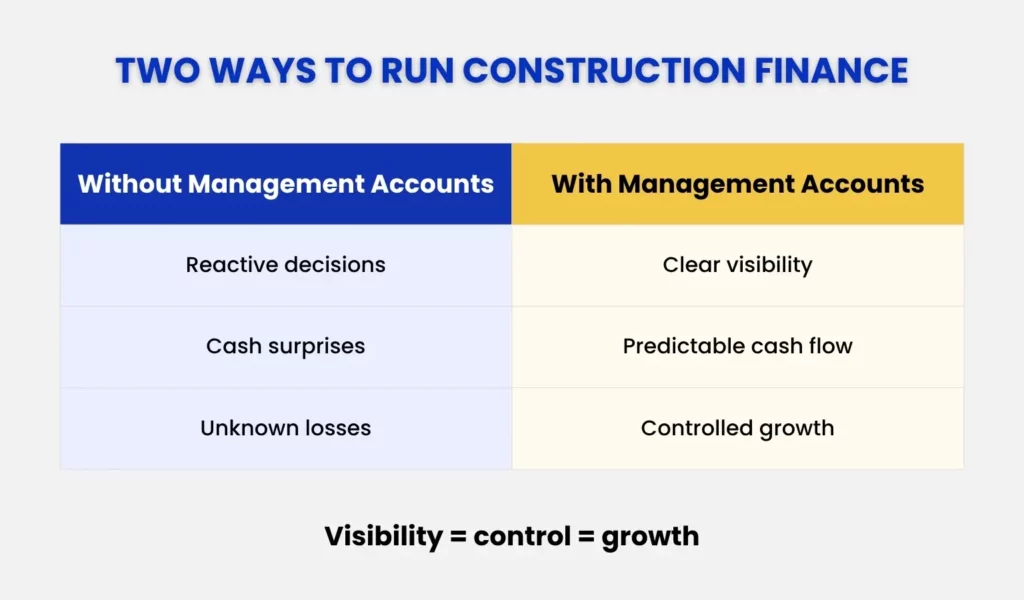

- Reactive Decision-Making: Only looking at the numbers when there is a crisis, rather than using them to steer the ship proactively.

- Failing to Reconcile CIS: Not checking that your CIS deductions match what HMRC has on file, leading to massive penalties and interest.

How to Get Started With Construction-Specific Management Accounts

There is no need to renovate everything in a single day. First, make sure your bookkeeping is “clean” (no “scratch” or leftover from previous books) and that each invoice is associated with a specific project. With project-level data, you’ll be able to start adding in WIP adjustments and cash flow forecasting.

The aim is to learn to move from ‘guessing’ to ‘knowing’. If you’re certain that you know where each penny is going, then you can make bold business decisions—such as whether you need that new foreman or whether you should invest in new plants and machinery. The first step is often a “Diagnostic Review” of your current systems to see where the data gaps are. This is possible only with the help of management accounts for construction companies.

Conclusion

Running a construction company without tailored management accounts is like trying to build a house without a blueprint. You might get lucky, but eventually, the structural flaws will show. By focusing on project-level profit, WIP, and cash flow, you give yourself the visibility needed to scale your business sustainably. In the fast-moving Hertfordshire market, the builders who win are those who know their numbers as well as they know their trade.

Serving Construction Businesses Across Hertfordshire – Julian Hobbs & Co.

At Julian Hobbs & Co., we specialise in helping Hertfordshire builders move beyond basic compliance and into strategic growth. We understand the local market, the nuances of the Home Counties supply chain, and the specific challenges of the UK construction industry. Let us help you build a more profitable future.

People Also Ask:

What should be in management accounts for a construction company?

A robust pack should include a Project-Level P&L, Work in Progress (WIP) valuations, a Retention tracker, CIS position reports, a Cash Flow forecast, and an Overhead absorption analysis. These elements work together to provide a 360-degree view of your financial health.

What is Work in Progress (WIP) and why does it matter in construction accounts?

WIP represents the value of work completed but not yet billed. It matters because construction projects often span months; WIP ensures your profit is recorded in the period the work actually happened, rather than just when the invoice was sent. This prevents “artificial” profits or losses in your monthly reports.

How often should a construction company prepare management accounts?

At a minimum, you should review these monthly. In a fast-moving industry like construction, waiting for quarterly or year-end figures is often too late to fix a failing project. Monthly reviews allow you to catch overspending before it spirals out of control.

How does CIS affect management accounts for a contractor?

CIS (Construction Industry Scheme) affects your cash flow and liability. Your accounts must accurately reflect the tax deducted from subcontractors and the tax withheld from your own payments by contractors to ensure you are meeting HMRC requirements. Failure to manage this correctly can lead to significant fines and cash flow disruptions.

Can a small building company benefit from management accounts?

Absolutely. Even for small firms, knowing which jobs are profitable and having a clear view of upcoming cash requirements can be the difference between growth and insolvency. It also makes your business much more attractive to lenders if you ever need to finance new equipment or vehicles.

What is a typical gross margin for a construction company in the UK?

This varies by sector (residential vs. commercial), but many UK builders aim for a gross margin between 15% and 25%. Management accounts help you see if you are hitting these targets and, more importantly, why you might be missing them.

What is the best accounting software for construction management in the UK?

Xero is widely considered the best accounting software for construction management due to its ease of use and built-in CIS features. Its ability to integrate with other apps makes it a flexible foundation for any growing construction firm.

Can Xero handle construction management accounts?

Yes, especially when set up correctly with tracking categories for different projects and utilising its CIS module for subcontractor management. It allows for real-time tracking that spreadsheets simply cannot match.