What is a Higher Rate Tax Payer? Tax Reliefs, Brackets and How It Impacts You

Table of Contents

Quick Brief

If your income tips into the higher rate tax band, your tax position changes quickly.

You do not pay 40% on everything you earn. But you do start paying 40% on the portion of income above the basic rate threshold.

Being a higher rate taxpayer affects more than just your salary. It impacts savings interest, dividend tax, pension relief, child benefit, and how efficient your planning needs to be.

This guide explains what it really means and what to watch out for.

What Does It Mean to Be a Higher Rate Tax Payer?

In the UK, income tax is charged in bands.

For most of the UK, you become a higher rate taxpayer when your taxable income exceeds the basic rate limit. That threshold is currently £50,270.

Income above that level is taxed at 40%, up to £125,140. Above that, the additional rate applies. Remember that you only pay 40% on the income above the threshold, not on your whole salary.

Taxable income includes salary, bonuses, rental income, pension income, self employed profits and some benefits.

Understanding the Higher Rate Tax Band: How UK Tax Slabs Work

The UK uses a progressive tax system. The first part of your income falls within your Personal Allowance which is £12,570 for most people.

The next slice is taxed at 20%. This is the basic rate band.

Once your taxable income exceeds £50,270, the excess over this amount is taxed at 40%.

If your income goes beyond £125,140, the additional rate of 45% kicks in on the excess over this amount.

The system works in slices. You move through bands gradually. Crossing into higher rate tax does not mean all of your income is suddenly taxed at 40%.

Income Tax for Higher Rate Taxpayers: How Much You Will Pay

As a higher rate taxpayer, the portion of your income above £50,270 is taxed at 40%. For example, if your taxable income is £60,000, you pay 40% on roughly £9,730 of it.

Your effective tax rate will be lower than 40% because part of your income is taxed at 20% and part may be tax free. However, once you are in the higher rate band, tax planning becomes more important.

How Does Personal Savings Allowance (PSA) Affect Higher Rate Tax Payers?

Your Personal Savings Allowance reduces once you become a higher rate taxpayer.

Basic rate taxpayers usually get £1,000 of savings interest tax free but higher rate taxpayers usually get £500 and additional rate taxpayers get none.

This means you can start paying tax on savings interest much sooner once your income crosses the higher rate threshold. With higher interest rates in recent years, many higher rate taxpayers are now exceeding their £500 allowance without realising it (see our guide on HMRC savings account tax warnings).

If your savings interest is close to or above the allowance, consider using tax-efficient options such as ISAs – read our guide to tax-free savings accounts in the UK.

Tax Reliefs for Higher Rate Tax Payers: Maximise Your Benefits

One of the advantages of being a higher rate taxpayer is the level of tax relief available.

Pension contributions are a good example.

If you contribute to a pension, you can receive tax relief at 40% on the portion of income taxed at the higher rate. This can significantly reduce your effective tax bill.

Gift Aid donations also provide additional relief. If you make charitable donations, you can claim back the difference between basic rate and higher rate tax on the grossed-up donation.

Other reliefs may apply depending on your circumstances, including relief for trading losses or certain investment schemes.

Planning becomes much more valuable once you cross into the 40% band.

What Happens Once You Cross the £150,000 Threshold?

Above £125,140, the additional rate of 45% applies. There is also a sharp increase in tax pressure between £100,000 and £125,140.

In that band, your Personal Allowance is gradually withdrawn. For every £2 of income above £100,000, you lose £1 of Personal Allowance. This creates an effective tax rate of 60% on income within that range.

This is often referred to as the tax trap zone.

Careful pension contributions or charitable donations can help reduce taxable income and restore some of the allowance.

Practical Tips for Managing Taxes as a Higher Rate Taxpayer

If you are in the higher rate band, small adjustments can make a big difference.

Review your pension contributions. Increasing them may reduce your taxable income.

Consider salary sacrifice arrangements if available.

Use your ISA allowance to protect savings interest from tax.

Check your tax code to ensure it is correct.

If you receive rental income or dividends, review the overall structure and ownership.

Being proactive often saves more than reacting later.

How National Insurance Affects Higher Rate Tax Payers

National Insurance works differently from Income Tax.

For employees, National Insurance drops from the main rate to a lower rate once earnings exceed a certain threshold.

This means that although Income Tax increases to 40%, National Insurance may reduce on higher earnings. For the self employed, Class 4 National Insurance also reduces above certain profit levels.

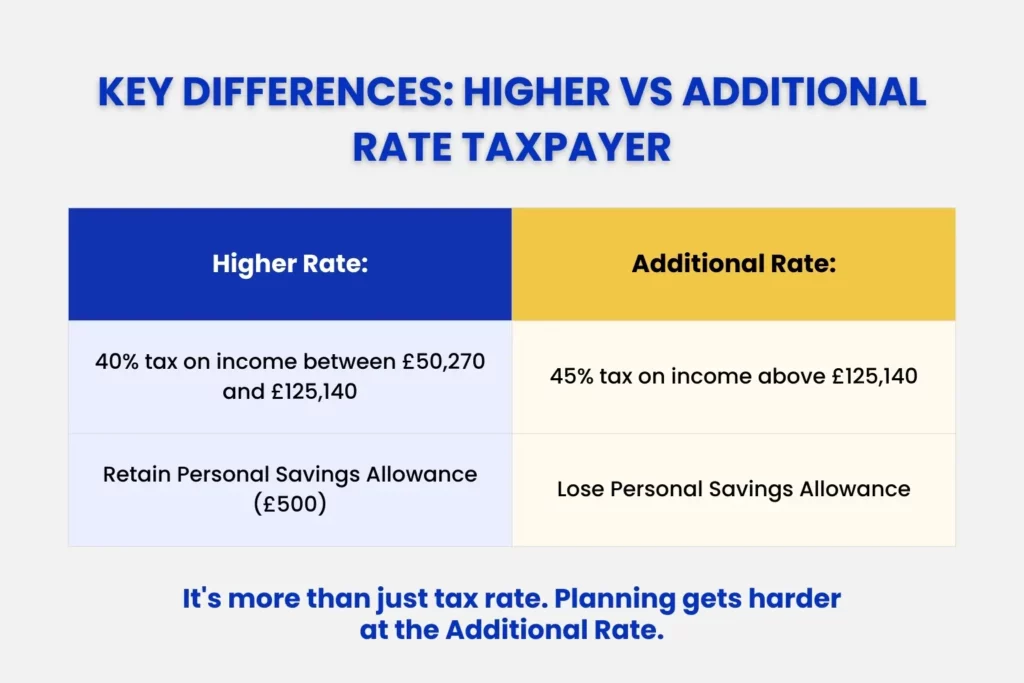

How Does a Higher Rate Tax Payer Compare with an Additional Rate Taxpayer?

A higher rate taxpayer pays 40% on income above £50,270 up to £125,140.

An additional rate taxpayer pays 45% on income above £125,140. Additional rate taxpayers also lose their Personal Savings Allowance entirely and may face tighter limits on certain reliefs.

The difference is not just 5%. It can affect allowances and planning options as well.

Common Mistakes to Avoid

Assuming all income is taxed at 40% once you cross the threshold.

Ignoring the impact on child benefit. The High Income Child Benefit Charge applies once income exceeds £60,000 in certain circumstances.

Forgetting to claim higher rate pension relief.

Overlooking the reduction in Personal Savings Allowance.

Not reviewing your tax code after a pay rise or bonus.

Small oversights can become expensive over time.

Conclusion

Becoming a higher rate taxpayer is not unusual. Many professionals, business owners and dual income households cross the £50,270 threshold.

The key is understanding how the system works and using the available reliefs effectively.

With the right planning, you can manage your tax position rather than letting it manage you.

Who qualifies as a higher rate tax payer in the UK?

Anyone whose taxable income exceeds £50,270 and falls below the additional rate threshold.

What is the current tax band for higher rate tax payers?

Income between £50,270 and £125,140 is taxed at 40%.

How much tax will I pay as a higher rate tax payer?

You pay 40% on income above the higher rate threshold, with lower rates applying to the rest.

What is the difference between a higher rate taxpayer and an additional rate taxpayer?

Higher rate taxpayers pay 40% on part of their income. Additional rate taxpayers pay 45% on income above £125,140.

Can higher rate taxpayers contribute to pensions to reduce their taxable income?

Yes. Pension contributions can reduce taxable income and provide higher rate tax relief.

How can I avoid paying tax on my savings as a higher rate taxpayer?

Using ISAs and managing your savings interest carefully can help reduce tax exposure. You can consider transferring assets to a spouse in certain circumstances to equalise your interest income.

What is higher rate tax payer pension relief and how does it benefit me?

It allows you to claim additional tax relief on pension contributions so that income taxed at 40% receives full relief.

Julian Hobbs

Julian Hobbs is the founder of Julian Hobbs & Co, a leading chartered accountancy firm in Hertfordshire. With a background from the University of Cambridge, Julian specialises in real-time business performance analysis, helping clients make informed financial and strategic decisions. Known for his forward-thinking approach, he combines expertise in accounting, tax planning, and advisory services to deliver actionable insights to businesses across the UK.