Quick Brief

Most people contributing to a pension assume that the government handles everything on their behalf. While this is mostly true for basic-rate taxpayers, higher-rate (40%) or additional-rate (45%) taxpayers must cover an additional 20% themselves, depending on the pension scheme. This is something where millions of UK earners lose hundreds of pounds every year.

Navigating this realm and understanding what higher rate pension tax relief is, who qualifies for it, and how the numbers work – will be exactly what this blog covers. From sole traders to directors and employees – this guide will aim to help you claim what is rightfully yours.

What Is Tax Relief?

Tax relief, in its simplest terms, is the government’s initiative to reduce the amount of tax you owe. When you contribute to pensions, donations and more, HMRC treat that money as if it were never taxed in the first place.

Think of it this way – Sarah, who is an employee with ATX Ltd, earns £100. In normal circumstances, the government would take £20 in income tax. But with tax relief like pensions – HMRC effectively hands the tax back, making your contribution cheaper than it looks on paper. It is not a loophole or grey area – it’s government policy deliberately built to help you save for your retirement.

What Is Pension Tax Relief?

Pension tax relief is when the government adds to your pension pot by giving you tax relief on your contributions.

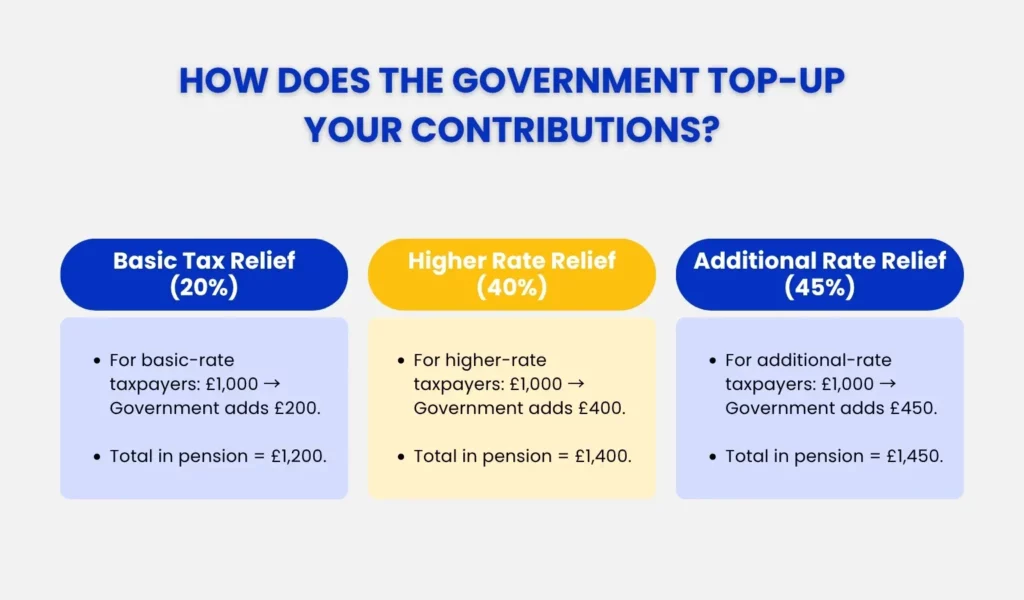

For every qualifying contribution to a registered pension scheme, HMRC tops it off based on the income tax rate you pay. For example, if you’re a basic rate taxpayer and you contribute £1,000 to your pension, the government will add £200 (20%) as tax relief- making your total contribution to £1,200.

This relief is even greater for higher rate and additional-rate taxpayers.

| Your Tax Band | Tax Rate | Total Relief | Net Cost of £100 into Pension |

| Basic Rate | 20% | 20% | £80 |

| Higher Rate | 40% | 40% | £60 |

| Additional Rate | 45% | 45% | £55 |

- Basic rate (20%) applies to taxpayers’ earnings from £12,570 to £50,270.

- And, a higher rate (40%) on earnings between £50,271 and £125,140.

While the 20% basic relief is added automatically to your pension, above this (higher & additional rate) depends on the type of pension scheme you’re in – not your income levels.

What Is Higher Rate Pension Tax Relief?

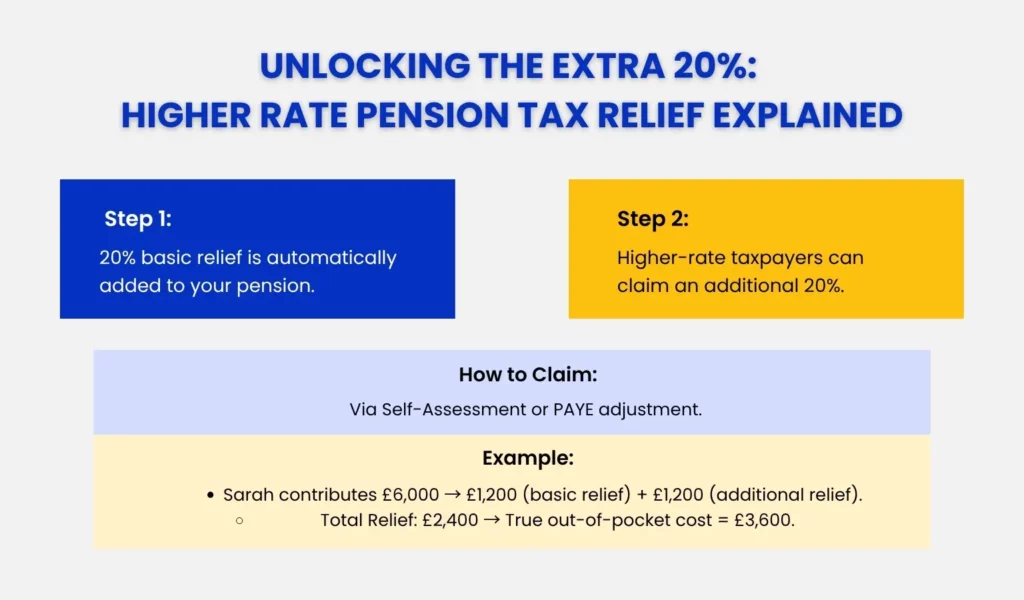

Higher rate pension tax relief is the additional 20% relief that higher rate taxpayers can claim on top of the automatic 20%. In total, this brings the government’s contribution up to 40%.

However, it’s important to note that the additional 20% isn’t automatically added to your pension pot. You must claim it through self assessment return or a PAYE adjustment.

Let’s once again bring back the example of Sarah.

She is earning £55,000 and wants to make pension contributions of £6,000. With basic relief, she gets 20% relief, i.e. £1200. Since she is a higher rate taxpayers, she gets an additional 20% – £1200, totalling to £2400 tax relief.

In the end, her true out-of-pocket cost comes to just £3,600 (£6,000 − £2,400 tax relief), while her pension pot totals £6,000.

There is a catch, however. With a net pay arrangement, the full relief is applied automatically (contributions are deducted from gross salary before tax is calculated). Meanwhile, with relief at source scheme, the additional 20% sits with HMRC, and she has to actively claim it to get 40% tax relief.

Who Gets Higher Rate Pension Tax Relief?

Higher Rate Pension Tax Relief is available to anyone whose earnings (including salary, rental income, dividends and other taxable sources combined) exceed £50,270 in 2026/27.

You must also be under 75 and contributing to a registered UK pension scheme. Your annual allowance also has to be under £60,000.

How Do I Calculate Pension Contributions?

Calculation of pension contributions is pretty straightforward, depending on your contribution type – workplace pension or a personal pension scheme.

- Workplace Pension: This is further divided into relief at source scheme, net pay arrangement scheme and a salary sacrifice scheme.

- With relief at source – you need to claim an additional 20% through self assessment return or by adjusting your PAYE code.

- As for the net pay arrangement scheme – your gross contribution is directly deducted from your salary before tax. No need for top-up calculation or claiming via self assessment or adjustment of PAYE code. Ex: Sarah’s taxable income becomes £55,000 − £6,000 = £49,000 (there is a reduction).

- With salary sacrifice, your employer deducts contributions before tax and National Insurance, making it the most tax-efficient of the three. Sarah’s taxable income not only reduces to £49,000 but also saves her National Insurance – which she can pocket each year.

- With relief at source – you need to claim an additional 20% through self assessment return or by adjusting your PAYE code.

- Personal Pension/SIPP: Here, the contributions are made by you, and you decide on your pension provider. Fundamentals are the same – basic rate 20% relief is automatically applied, meanwhile, for higher rate, you need to claim via self assessment.

How to Calculate Higher Rate Tax Relief on Pension Contributions?

Let us run through Sarah’s full calculation, whose gross salary is £55.000 and wants to make a pension contribution of £6,000 :

Step 1: Sarah’s Tax Bill Without Any Pension Contribution:

| Personal Allowance (0%): £12,570 –> £0 |

| Basic Rate (20%)up to £50,270: → £7,540 (37700*0.2) |

| Higher Rate (40%): (£55,000 − £50,270) → £4,730*0.4 → £1,892 |

| Total Income Tax: £9,432 |

Step 2: Sarah Contributes at Relief at Source Scheme:

Sarah pays £4,800, not £6,000. Because intial 20% is directly from HMRC.

Hence – 6000*20% = £1200

→ £6,000 – £1200 = £4800.

Ultimately, her gross in pension pot will total 6,000.

Step 3: Sarah Claims the Additional 20% via Self Assessment:

| Gross contribution: £6,000 |

| Additional 20% relief: £1,200 ( she must claim this via self assessment) |

| Ultimately, her revised tax bill: £9,432 – 1200 =.£8,232 |

Final Summary:

| Out of pocket: £4,800 (before claiming additional 20% = £1200 via self assessment) |

| Added by Government (auto): +£1,200 |

| Higher rate relief claimed: +£1,200 – must be claimed via self assessment |

| Total pension tax relief: £2,400 |

| Sarah’s true net cost: £3,600 |

How Do Sole Traders Claim Higher Rate Relief?

Unlike employees whose payroll is processed through the PAYE system, sole traders’ pension contributions must come from registered personal pensions/SIPPs.

The pension provider will then claim 20% basic rate relief and add it to the pot automatically. If the trading profit exceeds £50,270, an additional 20% higher rate will apply – which can then be claimed through self assessment tax return.

Remember, you can only claim relief up to your annual allowance – £60,000 or 100% of your net trading profits, whichever is lower. Higher than it – will trigger tax charges from HMRC on the remaining profits.

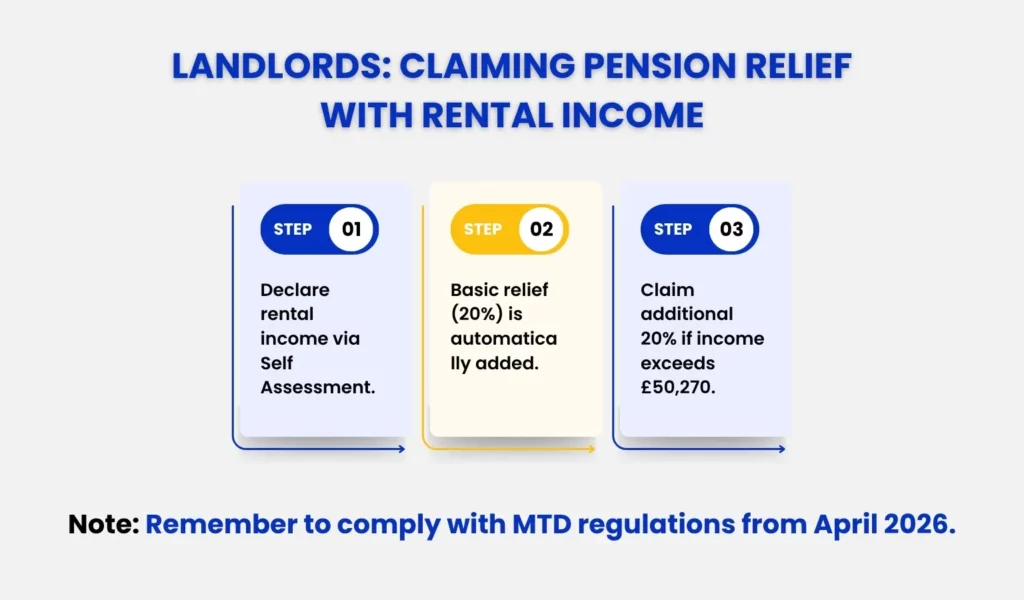

How Do Landlords Claim Pension Relief?

Most landlords already file Self Assessment return to declare rental income. This makes claiming pension relief relatively simple since it’s included in the same return. When this added rental income pushes total taxable income to above £50,270 threshold – you can qualify for 40% tax relief (20% basic which is automatic, and additional 20% for higher-rate taxpayers).

Remember to keep in mind the recent MTD changes which will come into effect from April 2026. Read our MTD for Landlords guide to know how you can safely comply while claiming pension reliefs.

How Do Dividend Directors Claim via PAYE?

Dividend directors who use a mix of salary plus dividends may often find their total cross the higher rate threshold. These higher-rate taxpayers can then claim additional 20% tax relief through PAYE or self assessment.

Since we are discussing the claim via PAYE even though declaring dividend income through self assessment is more common; with PAYE , HMRC will make adjustments to the tax code to reflect pension contributions, thereby reducing monthly PAYE deductions without having to wait until year end.

How Do I Claim via Self Assessment?

Claiming higher rate pension tax relief through self assessment is simpler than it sounds. Here’s the process – step-by-step:

- Register for Self Assessment with HMRC if you do not already file a return.

- Obtain your gross contribution figure from your pension provider. This is your personal payments plus the 20% basic relief already added.

- Complete your Self Assessment return via your HMRC online account.

- HMRC will either reduce your tax bill for the year or issue a repayment, depending on whether you have already overpaid through PAYE or self-assessment payments on account.

- If you have missed previous years, you can reclaim up to four tax years back

If Self Assessment registration feels daunting, contact your local accountant or HMRC to help with self assessment registration and claim.

Conclusion

Higher rate pension tax relief gives you an extra 20% relief on top of the basic 20%, allowing you to save even more for your retirement. The only condition is that, for most people in a relief at source scheme – you have to ask for it. HMRC will not chase you. You need to be proactive to claim additional tax relief via self assessment or PAYE adjustments, whichever is more straightforward and simple.

Why Choose Julian Hobbs & Co for Your Pension Relief?

At Julian Hobbs & Co. we specialise in proactive pension and tax planning for higher earners, sole traders, landlords and dividend directors. We make sure you claim full entitlements- correctly and efficiently year after year.

From helping you register for self assessment, to adjusting your PAYE and even reviewing multiple years of potentially unclaimed relief – our help extends beyond compliance – providing personalised services that grow with you.

Get in touch with us and find out exactly how much higher rate pension tax relief you are entitled to, this 2026/27 tax year.

People Also Ask:

What is higher rate pension tax relief?

Higher rate pension tax relief is an additional 20% relief available to higher rate taxpayers earnings between £50,271 and £125,140.

Do sole traders get higher rate relief?

Yes, sole traders can get higher rate relief if their net trading profits above £50,270. Then additional relief of 20% can further be claimed via self assessment.

How to claim higher rate tax relief on pension contributions?

The most common route is through a Self Assessment tax return. You just have to enter your gross pension contribution (your personal payments plus the 20% already added by your provider), and HMRC calculates the relief owed.

Alternatively, you can also contact HMRC to request a PAYE tax code adjustment.

Do dividend directors get higher rate pension relief?

Yes, provided their combined income – salary plus dividends – exceeds £50,270. They can then claim for higher rate pension tax relief through self assessment tax return or PAYE (tax code adjustments), whichever is applicable.

What is the pension annual allowance for higher rate taxpayers?

For 2026/27, the standard annual allowance is £60,000 or 100% of your UK earnings – whichever is lower. Unused allowances from the previous three tax years can also be carried forward.

Do I get 40% pension relief automatically?

It depends on your pension scheme. If you’re on a workplace pension scheme – primarily the net pay arrangement type – you receive full 40% relief without any further action. Whereas, if you use relief at source scheme – additional 20% relief should be claimed through self assessment.