If you sell an asset for more than you paid for it, Capital Gains Tax (CGT) will apply to the profit. But there is an annual exemption, and a range of reliefs, that can significantly reduce what you owe.

This article explains what capital gains tax exemption is and which reliefs you should know about for 2026/27 and beyond.

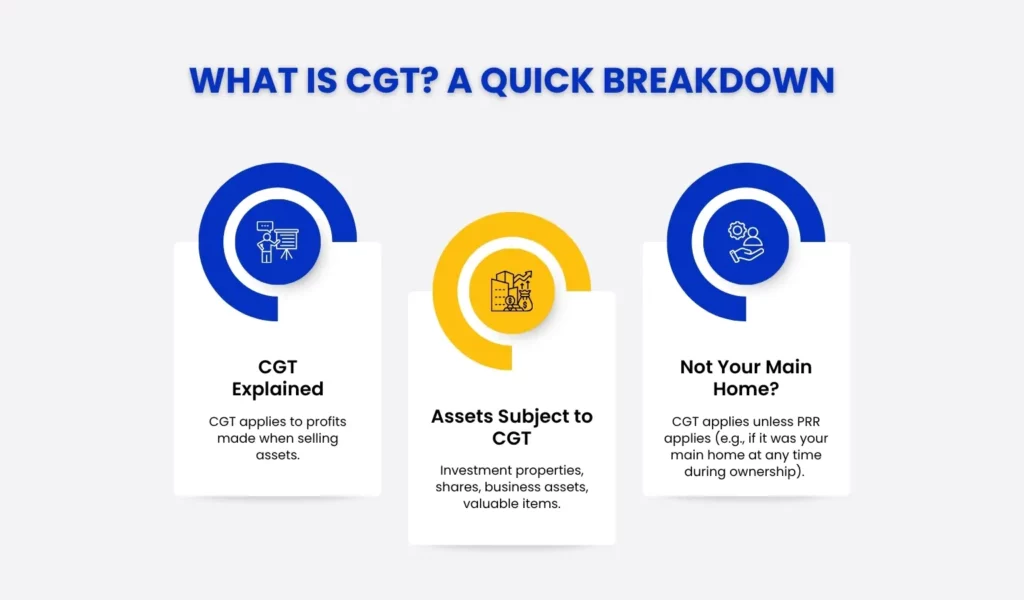

Setting the Foundation: What is Capital Gains Tax?

CGT is the tax you pay on the gain when you dispose of a qualifying asset. The gain is simply the profit made (ie the sales price less the purchase price assuming its value went up). You are not taxed on the full sale price, only on what you made (the profit) above your original cost.

Common assets subject to CGT include investment properties, shares, business assets, and certain personal possessions worth over £6,000.

Your main home is usually exempt through Private Residence Relief, which we cover below.

What is Capital Gains Tax Exemption?

Each tax year, every individual has an Annual Exempt Amount. This is the amount of gains you can make before Capital Gains Tax is charged.

For 2026/27, the Annual Exempt Amount is £3,000. Gains below this figure are not taxed.

This exemption cannot be carried forward to the next tax year. If you don’t use it, you lose it! This brings in potential CGT planning points for example selling some shares with inherent gains each year to utilise the annual exemption.

Couples and civil partners each have their own separate exemptions. Therefore, a couple acting efficiently can utilise up to £6,000 of annual gains and have them covered by the exemption.

How to Claim Capital Gains Tax Exemption

The Annual Exempt Amount applies automatically to UK residents (individuals not companies of course). You do not need to apply for it.

To make the most of it, you need to:

- Keep records of what you paid for assets and when

- Track any improvement costs, which can be deducted from your gain

- Report gains above the exempt amount through Self Assessment

- For residential property, report and pay CGT within 60 days of completion

If your total gains in a tax year stay below £3,000, you have nothing to pay – they are all covered by the Annual Exemption. But, bear in mind that you may still need to report them on your tax return even though no tax is owing.

Key CGT Reliefs You Should Know About

Beyond the Annual Exempt Amount, there are several other reliefs that can reduce or eliminate CGT entirely.

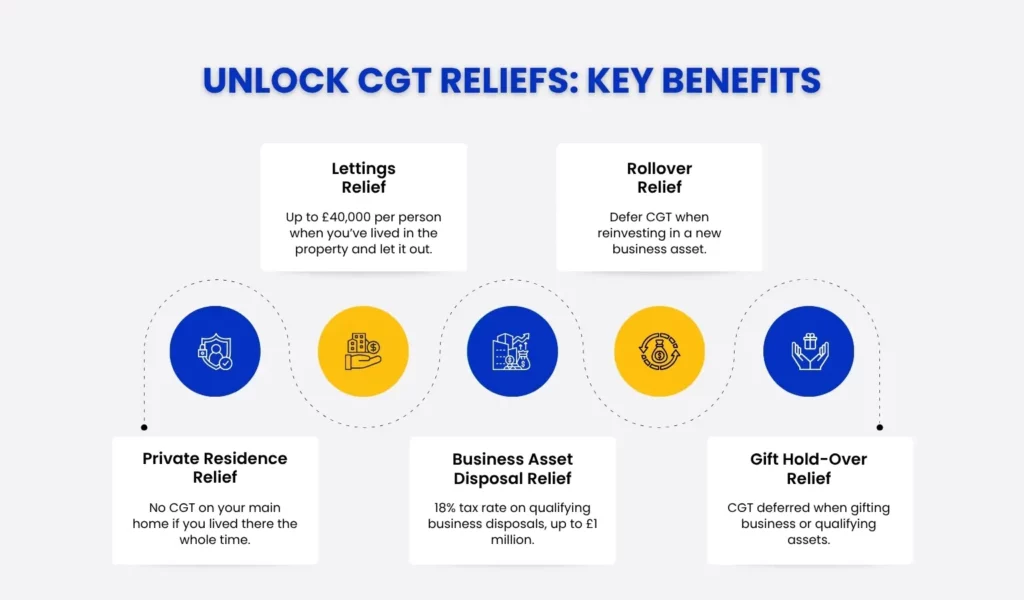

Private Residence Relief

If you sell your main home, you are exempt from CGT on the full gain if it was your main home for the duration of ownership. This is one of the most valuable reliefs available as your home will most likely be the largest asset you will own.

If you have let the property or used a part of it exclusively for business, the relief may be restricted. You should take advice before selling if you have rented your home out ever, or have owned a second home (even if not rented out).

Lettings Relief

Lettings Relief can apply where you have lived in a property as your main home and also let it out during your period of ownership. However, the rules changed significantly in April 2020.

Letting Relief now only applies where you were living in the property at the same time as your tenant, for example in a lodger arrangement. It is no longer available for properties you let out while not living there yourself.

Where it does apply, Letting Relief is worth a deduction from of the gain of up to £40,000 per person, capped at the amount of PRR available and the gain attributable to the letting period.

Business Asset Disposal Relief

Formerly called Entrepreneurs’ Relief, this reduces the CGT rate to 18% (from April 2026) on qualifying business disposals, up to a lifetime limit of £1 million.

To qualify, you must have owned the business for at least two years and meet certain conditions as an officer or employee.

Investors’ Relief

Similar to Business Asset Disposal Relief but aimed at external investors in unlisted trading companies. The same preferential rate applies, with a separate lifetime limit.

Gift Hold-Over Relief

If you give away a business asset or certain other qualifying assets, you can defer the CGT. The gain is effectively passed on to the recipient, who will pay CGT when they eventually sell.

Rollover Relief

If you sell a business asset and reinvest the proceeds into a replacement asset, you can defer the CGT gain. Useful for businesses that are reinvesting rather than cashing out.

The Impact of CGT Exemption on Trusts and Estate Planning

Trusts have a much smaller Annual Exempt Amount than individuals, currently half the personal exemption. This can lead to higher tax costs when trust assets are disposed of.

When someone dies, assets are usually rebased to their market value at the date of death. This means the beneficiary inherits without the deceased’s accumulated gains, which can be a significant tax advantage.

If estate planning is a priority, reviewing CGT exposure alongside Inheritance Tax is always worthwhile.

How to Calculate Capital Gains Tax with the Exemption Applied

Here is a simple example.

You sell a buy-to-let property and make a gain of £25,000. You deduct the Annual Exempt Amount of £3,000, leaving a taxable gain of £22,000. If you are a higher rate taxpayer, CGT on residential property is currently charged at 24%. Your CGT bill would be £5,280.

If your spouse or civil partner jointly owns the property, you can each use your own £3,000 exemption, reducing the combined taxable gain to £19,000 and saving a further £720 in tax.

To better understand how CGT is calculated on property sales and how reliefs can impact your tax, check out our step-by-step guide for homeowners and investors.

What to Expect from CGT Exemptions in 2026/27 and Beyond

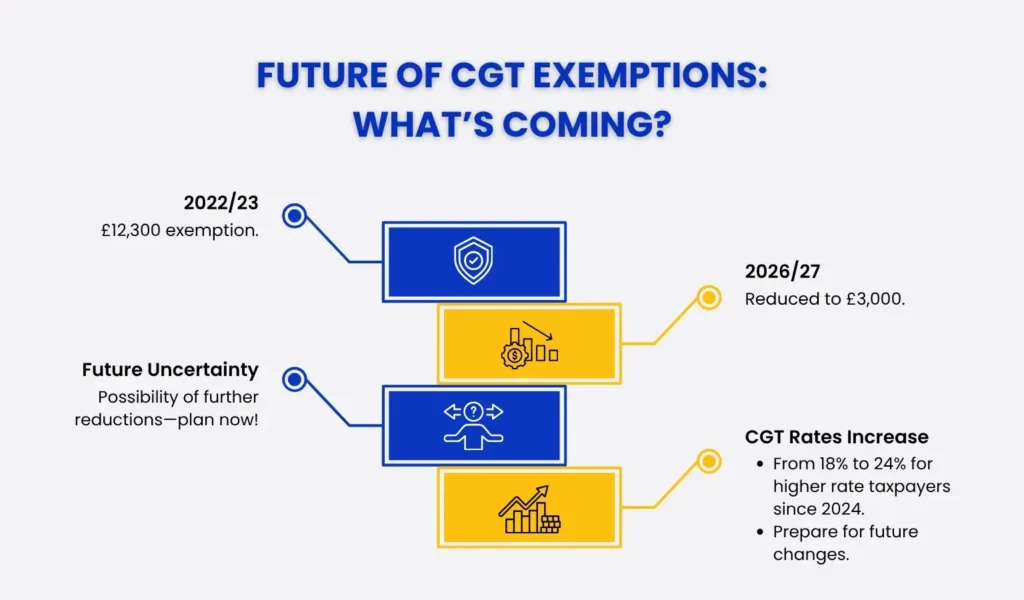

The Annual Exempt Amount has fallen sharply in recent years. It stood at £12,300 in 2022/23 and has been cut to £3,000. The government has not announced further reductions, but there is no guarantee the allowance will not be cut further.

The CGT rates on most assets increased in October 2024 to align more closely with income tax. However, CGT rates are still well below income tax rates in many cases, and there is the possibility of further increase in the same.

With a smaller exemption and higher rates, planning ahead is more important than ever.

Final Thoughts

The Capital Gains Tax exemption is a useful tool, but with the annual allowance now at just £3,000, it does not go as far as it once did. The reliefs available, particularly Private Residence Relief and Business Asset Disposal Relief, can be far more valuable.

The key is knowing which reliefs apply to your situation and planning around them early, not after a disposal has already happened.

How Julian Hobbs & Co Can Help You

We help individuals, investors, landlords and business owners understand their CGT position and plan disposals in a tax efficient way.

If you are thinking about selling an asset and want to understand what you might owe, book a call with our team. We will walk you through the numbers clearly and make sure you are not paying more than you need to.

People Also Ask:

What is Capital Gains Tax Exemption for 2026/27?

The Annual Exempt Amount for 2026/27 is £3,000. Gains below this threshold are not subject to CGT.

How do I qualify for CGT Exemption in the UK?

The exemption applies automatically to UK resident individuals. You do not need to claim it. You just need to keep accurate records and report gains above the threshold through Self Assessment.

What are the key Capital Gains Tax reliefs available?

The main reliefs are Private Residence Relief for your main home, Business Asset Disposal Relief for qualifying business sales, Gift Hold-Over Relief, Investors’ Relief, and Rollover Relief for reinvested business assets.

Can I claim CGT Exemption on the sale of my home?

In most cases, yes. If the property has been your main residence throughout the period of ownership, Private Residence Relief should cover the full gain. Partial relief may apply if you let the property or used it for business. Always seek advice.

What CGT reliefs apply to trusts?

Trusts have a reduced Annual Exempt Amount, currently half the individual allowance. Certain other reliefs may apply depending on the type of trust and the assets held.

Is agricultural land exempt from Capital Gains Tax in the UK?

Agricultural land is not automatically exempt, but Agricultural Property Relief may reduce the Inheritance Tax position. For CGT, Rollover Relief or Gift Hold-Over Relief may apply in certain circumstances. Specialist advice is recommended.

Are gold coins exempt from CGT?

UK legal tender gold coins, such as Sovereigns, are exempt from CGT because they are classed as sterling currency. Foreign gold coins and gold bullion are not exempt.

How do I calculate CGT with the exemption applied?

Start with your total gain, deduct your £3,000 Annual Exempt Amount, then apply the relevant CGT rate to the remaining taxable gain. The rate depends on whether you are a basic or higher rate taxpayer and the type of asset.