Introduction to Capital Gains Tax on Property

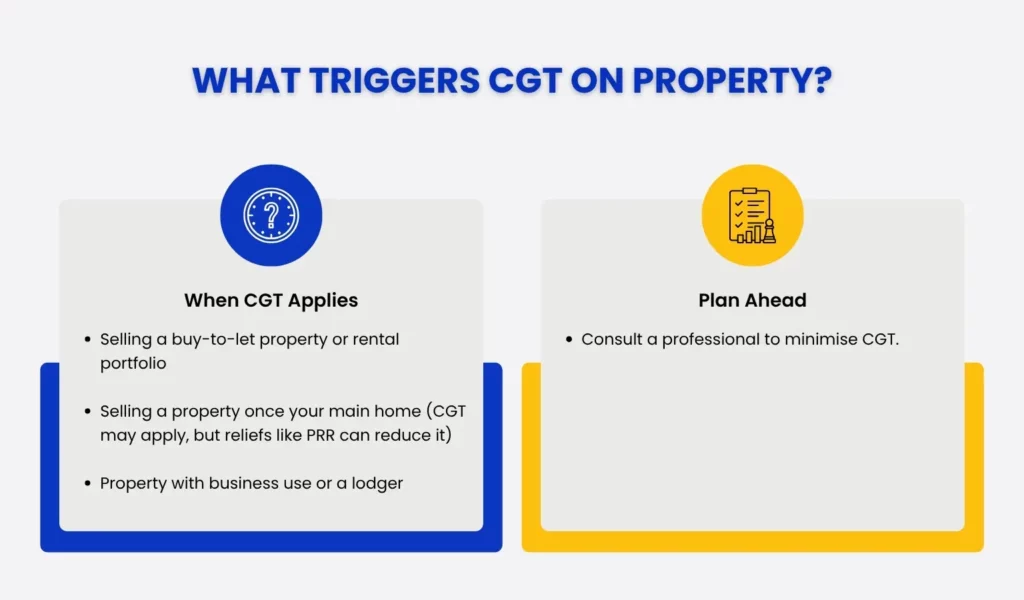

Selling a property in the UK can trigger a tax liability that catches many people off guard. Capital Gains Tax (CGT) applies when you sell a property that is not your main home, and the rules are more detailed than they first appear.

If you are selling a buy-to-let, disposing of a rental portfolio, or selling a property that you have lived in and let out at different times, understanding how CGT works before you complete a sale can save you a significant amount of money.

This guide takes you through how to calculate capital gains tax on property, what reliefs are available, and what steps you need to take to report and pay any tax owed.

Key Factors that Impact CGT on Property Sales

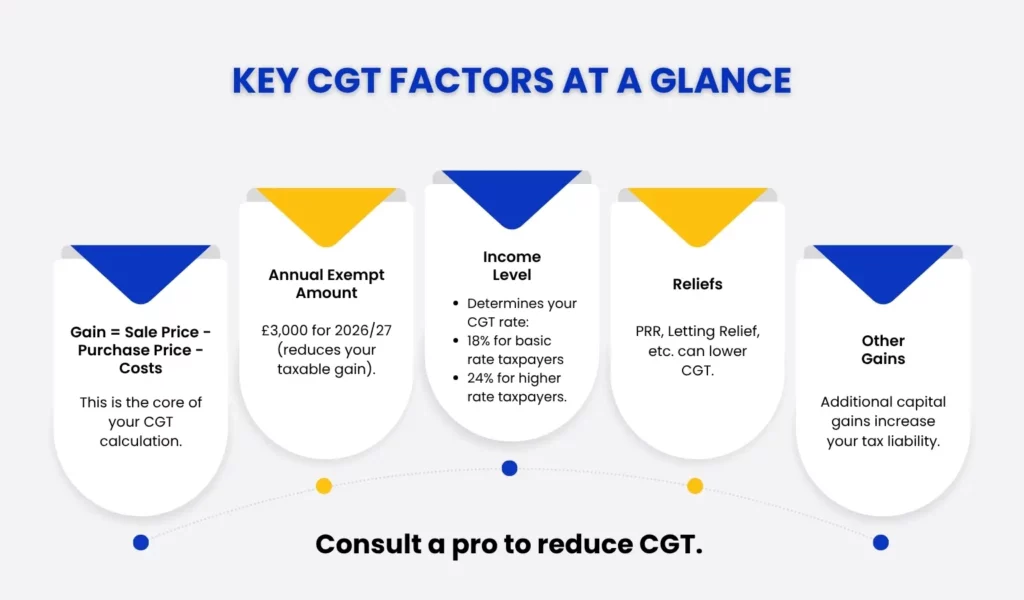

Several variables determine how much CGT you will pay when selling a property. The main ones are:

- The gain you have made, which is broadly the sale price minus the purchase price and allowable costs

- Your Annual Exempt amount, currently £3,000 for the 2026/27 tax year

- Your level of income, which determines which CGT rate applies to you

- Whether any reliefs reduce or eliminate the chargeable gain

- Whether you have made other capital gains in the same tax year

Getting these figures right is very important as CGT on property can easily run into tens of thousands of pounds on a typical sale. Planning ahead and understanding the rules gives you the best chance of managing the liability effectively.

UK CGT Rates for Property

For residential property, CGT rates are higher than for most other assets. The rates for the 2026/27 tax year are:

- 18% if you are a basic rate taxpayer

- 24% if you are a higher or additional rate taxpayer. (Learn how being a higher-rate taxpayer affects your tax liability and reliefs in our detailed guide)

To work out which rate applies, you add your taxable gain to your income for the year. If the combined total keeps you within the basic rate band, you pay 18%. If any part of the gain falls into the higher rate band, that portion is taxed at 24%.

Example: If your income is £40,000 and your taxable gain is £30,000, the first £10,270 of the gain uses up the remaining basic rate band and is taxed at 18%. The remaining £19,730 is taxed at 24%.

Special Cases: Overseas Property

If you own property abroad, UK CGT may still apply if you are a UK resident. The calculation follows the same principles, but you will also need to consider the tax rules in the country where the property is located. Double tax treaties between the UK and other countries can affect how much tax is due overall. This is an area where specialist advice is particularly valuable.

Understanding Capital Gains Tax Exemptions and Reliefs

Several reliefs can reduce or eliminate a CGT liability on property. Knowing which ones apply to your situation is one of the most important steps in the process.

Private Residence Relief

Private Residence Relief (PRR) is the most valuable CGT relief available on property. It eliminates any gain made on your main home, provided you have lived there throughout your period of ownership.

You also receive an automatic final period exemption covering the last nine months of ownership, even if you were not living there at that point. This helps in situations where a property has been your home but you have moved out before selling.

If you have ever let out part or all of your home, or used part of it exclusively for business, PRR may be restricted. Periods of absence can also affect the relief, depending on the reason for the absence and whether HMRC accepts them as qualifying.

Letting Relief

Letting Relief can apply where you have lived in a property as your main home and also let it out during your period of ownership. However, the rules changed significantly in April 2020.

Letting Relief now only applies where you were living in the property at the same time as your tenant, for example in a lodger arrangement. It is no longer available for properties you let out while not living there yourself.

Where it does apply, Letting Relief is worth up to £40,000 per person, capped at the amount of PRR available and the gain attributable to the letting period.

Rollover Relief

Rollover Relief allows certain business owners to defer a capital gain by reinvesting the proceeds into a new qualifying business asset. It is not widely applicable to residential property investors, but may be relevant in some commercial property scenarios.

Incorporation Relief

If you transfer a property rental business into a limited company, Incorporation Relief may defer any CGT liability that would otherwise arise. This is a complex area and depends on the business meeting HMRC’s definition of a trading business, which is not straightforward for most property portfolios. Professional advice is essential before proceeding.

Principal Private Residence Relief for Joint Owners

Where a property is jointly owned, each owner applies PRR to their own share of the gain independently. This means that if one owner has lived in the property as their main home and the other has not, different amounts of relief will apply to each person’s portion of the gain.

Deferred Capital Gains Tax on Inherited Property

Inherited property is treated differently for CGT purposes. When you inherit a property, your base cost for CGT is the probate value at the date of death, not the original purchase price. This means that gains made during the deceased’s lifetime are effectively wiped out for CGT purposes, though they may have been subject to Inheritance Tax instead.

If you then sell the inherited property at a higher value, CGT applies only on any increase since the date of inheritance.

How to Calculate Capital Gains Tax on Property (Step-by-Step)

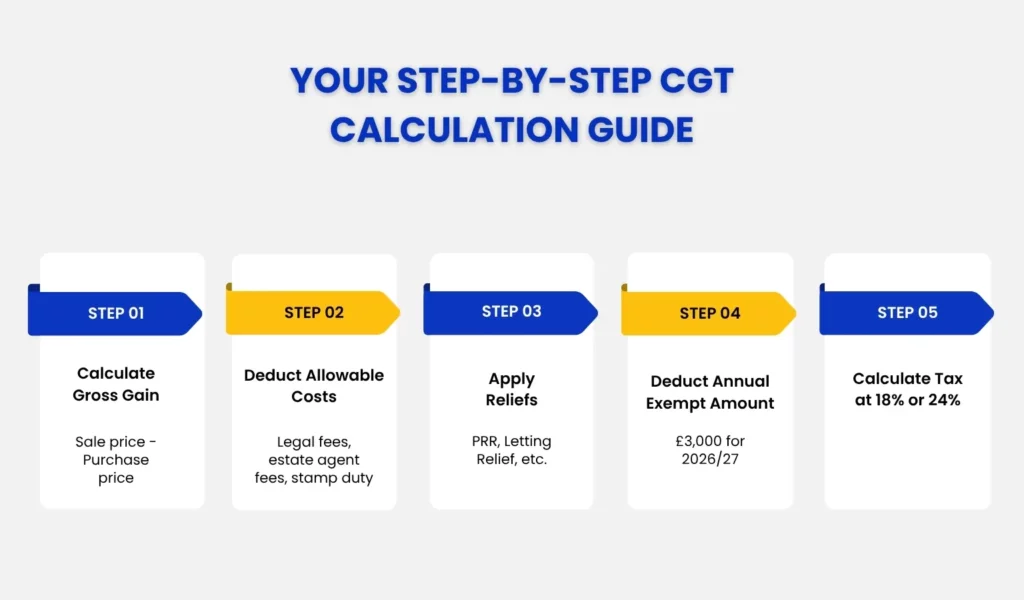

Here is a straightforward process for working out your CGT liability on a property sale.

- Work out your gross gain. Take the sale price and subtract the original purchase price.

- Deduct allowable costs. These include legal fees on purchase and sale, estate agent fees, stamp duty on purchase, and the cost of any capital improvements. Routine maintenance and repairs do not count.

- Deduct any applicable reliefs, such as Private Residence Relief or Letting Relief.

- Deduct your Annual Exempt Amount of £3,000 (2026/27).

- Add the remaining taxable gain to your income to determine which CGT rate applies.

- Calculate the tax owed at 18% or 24%, or a split of both if your gain straddles the basic and higher rate bands.

Keep clear records of all costs associated with buying, improving and selling the property. HMRC can ask for evidence of any deductions you claim.

Homeowners vs Investors: What You Need to Know

The CGT position of a homeowner selling their main residence is usually straightforward. If you have lived in the property throughout your ownership and it has always been your only home, PRR should cover the full gain and no CGT will be due.

The position becomes more complicated if you have:

- Owned more than one property at the same time

- Let the property out for any period

- Used part of the property exclusively for business

- Had extended periods of absence not covered by qualifying exemptions

For investors and landlords, CGT is a near-certainty on sale unless the property has been sold at a loss. The annual exempt amount of £3,000 provides only modest relief, and gains on property held for many years can be substantial.

“With MTD for Income Tax starting in April 2026, understanding how CGT will be reported in your quarterly updates is crucial. Reach out today for expert guidance on how the new system will impact your property sales and CGT reporting.”

Reporting and Paying CGT on Property Sales

The deadline for reporting and paying CGT on UK residential property is 60 days from the date of completion. This is a strict deadline and applies even if you are not yet sure of the final tax figure.

You report the gain using HMRC’s UK Property Reporting Service, which is separate from your Self Assessment tax return. You then pay any estimated tax within the same 60-day window.

You must also include the gain on your Self Assessment tax return for the relevant tax year. Any difference between the estimated tax paid within 60 days and the actual liability calculated on your return will be settled through the normal Self Assessment payment process.

Missing the 60-day deadline can result in an automatic penalty of £100, with further charges if the return remains outstanding. Interest is also charged on unpaid CGT from the day after the deadline.

Next Steps and Action Plan

If you are considering selling a property, or you have recently completed a sale, here is what you should do.

- Establish whether CGT applies to your sale and at what rate.

- Gather all records of purchase costs, improvement costs and sale costs.

- Identify any reliefs that may reduce your chargeable gain.

- Report any gain on UK residential property within 60 days of completion.

- Include the gain on your Self Assessment tax return.

- Speak to an accountant before the sale if possible, not after. Pre-sale planning can make a material difference to the outcome.

How Julian Hobbs & Co. Can Help with Your CGT Calculation

CGT on property is one of the areas where professional advice pays for itself. A small oversight in calculating your gain, missing an available relief, or failing to report on time can cost far more than the cost of advice.

We help homeowners, landlords and investors understand exactly what CGT applies to their sale, calculate the liability accurately, and ensure the reporting is done correctly and on time.

If you are planning a property sale or have recently completed one, get in touch with our team. We will review your position and make sure you are not paying more than you need to.

People Also Ask:

What is Capital Gains Tax on property in the UK?

Capital Gains Tax is a tax on the profit made when you sell an asset that has increased in value. On residential property that is not your main home, CGT rates are 18% for basic rate taxpayers and 24% for higher and additional rate taxpayers in 2026/27.

How do I calculate CGT when selling a property?

Start with the sale price, subtract the purchase price and all allowable costs, then deduct any applicable reliefs and your Annual Exempt Amount of £3,000. The remaining taxable gain is then taxed at the appropriate rate based on your income level.

Can I claim Private Residence Relief to reduce CGT?

Yes, if the property has been your main home throughout your period of ownership. PRR eliminates the gain attributable to the periods you lived there as your main residence. If you also let the property or had periods of absence, only part of the gain may be covered.

What is the deadline for reporting CGT on property sales?

You must report any CGT on UK residential property and pay the estimated tax within 60 days of the completion date. Missing this deadline can trigger an automatic £100 penalty and interest charges on any unpaid tax.

Do I need to pay CGT on inherited property?

Not at the point of inheritance. If you later sell the inherited property, CGT applies on any gain made since the date of death, using the probate value as your base cost. Gains made during the deceased person’s lifetime are not chargeable to CGT on the sale.

What exemptions and reliefs can reduce my CGT?

The main reliefs for property include Private Residence Relief, Letting Relief (in limited circumstances), and your Annual Exempt Amount of £3,000. The reliefs available to you depend on your specific circumstances.

How can Julian Hobbs & Co. help with calculating CGT on property sales?

We review your full position, calculate your gain accurately, identify all available reliefs, and handle the reporting to HMRC within the required deadlines. If you are planning a sale, we can advise you before you complete so that you have the best opportunity to manage your liability.